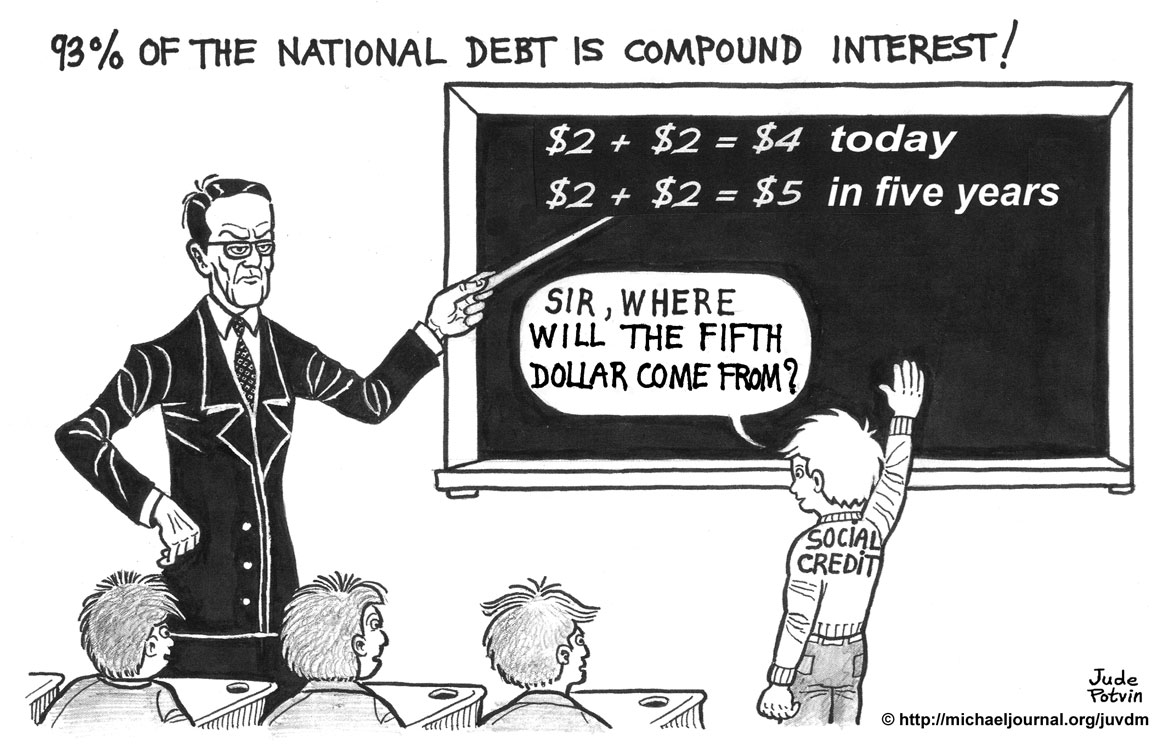

The cost of servicing the public debt increases proportionally to the debt, since it is a percentage of this same debt. To finance its debt, the Federal Government sells Treasury Bills and other bonds, most of them being bought by chartered banks.

As regards the sale of Treasury bonds, the Government is a stupid seller: it does not sell its bonds to the banks; it gives these bonds away to them, since these bonds cost the banks nothing: the banks do not lend the money; they create it. Not only do banks get something for nothing, but they also get interest on it.

Wright Patman

Wright Patman Marriner S. Eccles

Marriner S. EcclesOn September 30, 1941, a revealing exchange took place between Mr. Wright Patman, Chairman of the U.S. House of Representatives Banking and Currency Committee, and Mr. Marriner Eccles, Chairman of the Federal Reserve Board (the central bank of the U.S.A.) concerning a $2 billion monetary issue which the Bank created:

Mr. Patman: "How did you get the money to buy those $2 billion of Government securities?"

Mr. Eccles: "We created it."

Mr. Patman: "Out of what?"

Mr. Eccles: "Out of the right to issue money, credit."

Mr. Patman: "And there is nothing behind it, except the Government’s credit?"

Mr. Eccles: "We have the Government bonds."

Mr. Patman: "That’s right, the Government’s credit."

This puts us on the right track for a solution to the debt problem: if these bonds are based on the Government’s credit, why would the Government have to go through the banks to use its own credit?

It is not the banker who gives value to money, but the credit of the Government, of society. The only thing the banker does in this transaction is to make an entry in a ledger, writing figures which allow the country to make use of its own production capacity, its own wealth.

Money is nothing else but that: a figure — a figure which is a claim on products. Money is only a symbol, a creation of the law, according to Aristotle’s words. Money is not wealth, but the symbol that gives rights to wealth. Without products, money is worthless. So, why pay for figures? Why pay for something which costs nothing to make?

And since this money is based on the production capacity of society, this money also belongs to society. Then, why should society pay the bankers for the use of its own money? Why pay for the use of our own goods? Why doesn’t the Government issue its own money directly, without going through the banks?

Graham Towers

Graham TowersEven the first Governor of the Bank of Canada admitted that the Federal Government had the right to issue its own money. Graham Towers, who was Governor of the Bank from 1935 to 1951, was asked the following question, before the Canadian Committee on Banking and Commerce, in the spring of 1939:

Question: "Will you tell me why a government with the power to create money should give that power away to a private monopoly and then borrow that which Parliament can create itself, back at interest, to the point of national bankruptcy?"

Towers’ answer: "Now, if Parliament wants to change the form of operating the banking system, that is certainly within the power of Parliament."

Thomas Edison

Thomas EdisonU.S. inventor Thomas Edison said: "If our nation can issue a dollar bond, it can issue a dollar bill. The element that makes the bond good, makes the bill good also. The difference between the bond and the bill is that the bond lets the money brokers collect twice the amount of the bond and an additional 20 percent, whereas the currency pays nobody but those who contribute directly to Muscle Shoals in some useful way...

"It is absurd to say that our country can issue $30 million in bonds and not $30 million in currency. Both are promises to pay, but one fattens the usurers and the other helps the people. If the currency issued by the Government was no good, then the bonds would be no good either. It is a terrible situation when the Government, to increase the national wealth, must go into debt and submit to ruinous interest charges at the hands of men who control the fictitious value of gold."

Here are some questions the Social Crediters are often asked:

Question: Does the Government have the power to create money? Would this money be as good as that of the banks?

Answer: The Government has indeed the power to create, issue the money of our country, since it is itself, the Federal Government, that has given this power to the chartered banks. For the Government to refuse to itself a privilege it has granted to the banks, is the height of imbecility! Moreover, it is actually the first duty of any sovereign government to issue its own currency, but all the countries today have unjustly given up this power to private corporations, the chartered banks. The first nation that thus surrendered to private corporations its power to create money was Great Britain, back in 1694. In both Canada and the U.S.A., this right was surrendered in 1913.

Question: Is there not any danger that the Government might misuse this power and issue too much money, which would result in runaway inflation? Is it not preferable for the Government to leave this power to the bankers, in order to keep it away from the whims of the politicians?

Question: Is there not any danger that the Government might misuse this power and issue too much money, which would result in runaway inflation? Is it not preferable for the Government to leave this power to the bankers, in order to keep it away from the whims of the politicians?

Answer: The money issued by the Government would be no more inflationary than the money created by the banks: it would be the same figures, based on the same production of the country. The only difference is that the Government would not have to get into debt, or to pay interest, in order to obtain these figures.

On the contrary, the first cause of inflation is precisely the money created as a debt by the banks: inflation means increasing prices. The obligation for the corporations and governments that are borrowing to bring back to the banks more money than the banks created, forces the corporations to increase the prices of their products, and the governments to increase their taxes.

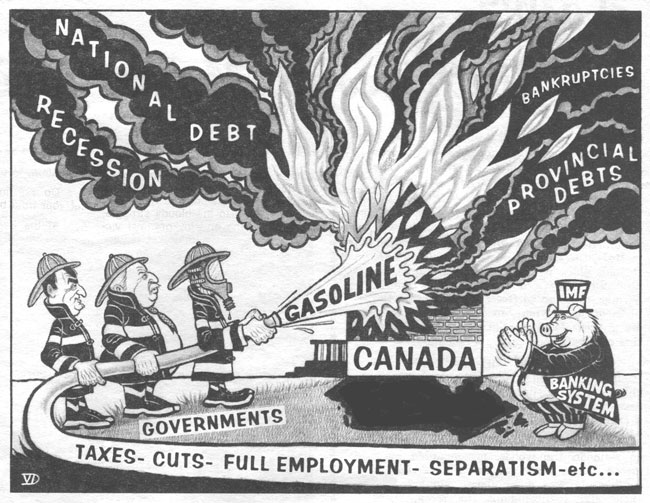

What is the means used by the present Governor of the Bank of Canada to fight inflation? Precisely what actually increases it, that is to say, to increase the interest rates! As many Premiers put it, "It is like trying to extinguish a fire by pouring gasoline over it."

It is obvious that if the Canadian Government decided to create or print money anyhow, without any limits, according to the whims of the men in office, without any relation with the existing production, there would definitely be runaway inflation. This is not at all what is proposed here by the Social Crediters.

What the Social Crediters advocate, when they speak of money created by the Government, is that money must be brought back to its proper function, which is to be a figure, a ticket, that represents products, which in fact is nothing but simple bookkeeping. And since money is nothing but a bookkeeping system, the only necessary thing to do would be to establish accurate bookkeeping:

The Government would appoint a commission of accountants, an independent organism called the "National Credit Office" (in Canada, the Bank of Canada could well carry out this job if ordered to do so by the Government). This National Credit Office would be charged with setting up accurate accounting, where money would be nothing but the reflection, the exact financial expression, of economic realities: production would be expressed in assets, and consumption in liabilities. Since one cannot consume more than what has been produced, the liabilities could never exceed the assets, and deficits and debts would be impossible.

In practice, here is how it would work: the new money would be issued by the National Credit Office as new products are made, and would be withdrawn from circulation as these products are consumed (purchased). (Louis Even’s booklet, A Sound and Effective Financial System, explains this mechanism in detail.) Thus there would be no danger of having more money than products: there would be a constant balance between money and products, money would always keep the same value, and any inflation would be impossible. Money would not be issued according to the whims of the Government nor of the accountants, since the commission of accountants, appointed by the Government, would act only according to the facts, according to what the Canadians produce and consume.

The best way to prevent any price increase is to lower prices. And Social Credit does also propose a mechanism to lower retail prices, called the "compensated discount", which would allow the consumers to purchase all of the available production for sale with the purchasing power they have at their disposal, by lowering retail prices (a discount) by a certain percentage, so that the total retail prices of all the goods for sale would equal the available total purchasing power of the consumer. This discount would then be refunded to the retailers by the National Credit Office. (This will be explained in Lesson 6.)

If the Government issued its own money for the needs of society, it would be automatically able to pay for all that can be produced in the country, and would no longer be obliged to borrow from foreign or domestic financial institutions. The only taxes people would pay would be for the services they consume. One would no longer have to pay three or four times the actual price of public developments because of the interest charges.

So, when the Government would discuss a new project, it would not ask: "Do we have the money?", but: "Do we have the materials and the workers to realize it?". If it is so, new money would be automatically issued to finance this new production. Then the Canadians could really live in accordance with their real means, the physical means, the possibilities of production. In other words, all that is physically possible would be made financially possible. There would be no more financial problems. The only limit would be that of the producing capacity of the nation. The Government would be able to finance all the developments and social programs demanded by the population that are physically feasible.

Under the present debt-money system, if the debt were to be paid off to the bankers, there would be no money left in circulation, creating a depression infinitely worse than any of the past. Let us quote again the exchange between Messrs. Patman and Eccles before the House Banking and Currency Committee, on September 30, 1941:

Mr. Patman: "You have made the statement that people should get out of debt instead of spending their money. You recall the statement, I presume?"

Mr. Eccles: "That was in connection with installment credit."

Mr. Patman: "Do you believe that people should pay their debts generally when they can?"

Mr. Eccles: "I think it depends a good deal upon the individual; but of course, if there were no debt in our money system..."

Mr. Patman: "That is the point I wanted to ask you about."

Mr. Eccles: "There wouldn’t be any money."

Mr. Patman: "Suppose everybody paid their debts, would we have any money to do business on?"

Mr. Eccles: "That is correct."

Mr. Patman: "In other words, our system is based entirely on debt."

How can we ever hope to get out of debt when all the money to pay off the debt is created by creating a debt? Balancing the budget is an absurd straitjacket. What must be balanced is the capacity to pay, in accordance with the capacity to produce, and not in accordance with the capacity to tax. Since it is the capacity to produce that is the reality, it is the capacity to pay that must be modeled on the capacity to produce, to make financially possible what is physically feasible.

John Paul II

John Paul IIPaying off one’s debt is simple justice if this debt is just. But if it is not the case, paying this debt would be an act of weakness. As regards the public debt, justice is making no debts at all, while developing the country. First, let us stop building new debts. For the existing debt, the only bonds to be acknowledged would be those of the savers; they who do not have the power to create money. The debt would thus be reduced year after year, as bonds come to maturity.

The Government would honour in full only the debts which, at their origins, represented a real expense on the part of the creditor: the bonds purchased by individuals, and not the bonds purchased with the money created by the banker, which are fictitious debts, created by the stroke of a pen. As regards Third-World countries’ debts, they are essentially owed to banks, which created all the money loaned to these countries. These same countries would therefore have no interest charges to pay back, and their debts would be, virtually, written off. Banks would lose nothing, since it is they that had created this money, which did not exist before.

Now we see how right are those who call for a reform of the financial system and the cancellation of debts, starting with Pope John Paul II, who wrote in his Apostolic Letter Tertio Millennio Adveniente, for the celebration of the Jubilee of the Year 2000:

"Thus, in the spirit of the Book of Leviticus (25:8-12), Christians will have to raise their voice on behalf of all the poor of the world, proposing the Jubilee as an appropriate time to give thought, among other things, to reducing substantially, if not cancelling outright, the international debt which seriously threatens the future of many nations."

St. Louis IX

St. Louis IXIt is Saint Louis IX, King of France, who said: "The first duty of a king is to coin money when it is necessary for the sound economic life of his subjects."

It is not at all necessary, nor to be recommended, that banks be abolished or nationalized. The banker is an expert in accounting and investing; he may well continue to receive and invest savings with profit, taking his share of profits. But the creation of money is an act of sovereignty which should not be left in the hands of a bank. Sovereignty must be taken out of the hands of the banks and returned to the nation.

Book money is a good modern invention that should be retained. But instead of it proceeding from a private pen, in the form of a debt, those figures, which serve as money, should come from the pen of a national organism, in the form of money destined to serve the people.

Therefore nothing is to be turned upside down in the field of ownership or investment. There is no need to abolish the current money and replace it with other kinds of money. All that is needed is that a social monetary organism add enough of the same kind of money to the money that already exists, according to the country’s possibilities and the population’s needs.

We must stop suffering from privations when there is everything needed in the country to bring comfort into every home. The amount of money in circulation must be measured according to the demand of the consumers for possible and useful goods.

It is therefore the producers and consumers as a whole, the whole of society, which, in producing goods to meet needs, should determine the amount of new money that an organism, acting in the name of society, should put into circulation from time to time, in accordance with the country’s developments.

Thus the people would recover their right to live full lives, in accordance with the country’s resources and the great possibilities of modern production.

Money should therefore be put into circulation according to the rate of production and as the needs of distribution dictate.

But to whom does this new money belong when it comes into circulation in the country? — This money belongs to the citizens themselves. It does not belong to the Government, which is not the owner of the country, but only the protector of the common good; nor does it belong to the accountants of the national monetary organism: like judges, they carry out a social function and are paid, according to law, by society for their services.

To which citizens? — To all. This money is not a salary. It is new money injected into the public, so that the people, as consumers, may obtain goods already made or easily realizable, which are awaiting only sufficient purchasing power for them to be produced.

One cannot imagine for one moment that the new money, which comes gratuitously from a social organism, only belongs to one or a few individuals in particular.

There is no other way, in all fairness, of putting this new money into circulation than by distributing it equally among all citizens without exception. Such a sharing also makes it possible to derive the maximum benefit from the money, since it reaches into every corner of the land.

Let us suppose that the accountant who acts in the name of the nation finds it necessary to issue another $1 million in order to meet the latest needs of the country. This issuance could take the form of book money, the inscription of figures in ledgers, as the banker does today.

Since there are 31 million Canadians and 1 billion dollars to share, each citizen would get $32.25. So the accountant would inscribe $32.25 in each citizen’s account. Such individual accounts could easily be looked after by the local post offices, or by branches, or by a bank owned by the nation.

This is the national dividend. Each citizen would have an extra $32.25 to his own credit, in an account bringing money into existence. This money would have been created and put into circulation by a national monetary organism, an institution especially established for this end by a law of Parliament.

Whenever it might become necessary to increase the amount of money in a country, each man, woman and child, regardless of age, would thus get his or her share of the new stage of progress that makes the new money necessary.

This is not payment for a job done, but a dividend to each one for his share in a common capital. If there is private property, there is also community property that all possess in the same way.

Here is a man who has nothing but the rags he is covered with. Not a meal in front of him, not a penny in his pocket. I can say to him:

"My dear fellow, you think you are poor, but you are a capitalist who possesses a great deal of things in the same way I and the Prime Minister do. The province’s waterfalls, the crown forests, are yours as well as mine, and they can easily bring you in an annual income.

"The social organization, which makes it possible for our community to produce a hundred times more and better than if we lived in isolation, is yours as well as mine, and must be worth something to you as it is to me.

"Science, which makes industry able to multiply production almost without human labour, is a heritage passed on to each generation, a heritage that is continuously growing; and you, who are a member of this generation just as I am, should have a share in this legacy, just as I do.

"If you are poor and naked, my friend, it is because your share has been stolen from you and put under lock and key. When you have no food, it is not because the rich eat all the grain in the land; it is because your share is still lying in the grain elevators. You have been deprived of the means of getting that grain.

"The Social Credit dividend will ensure that you get your share, or at least a major portion of it. A better administration, freed from the financiers’ influence and able to cope with these exploiters of men, will see to it that you get the rest.

"It is also this dividend that will recognize you as a member of the human species, in virtue of which you are entitled to a share of this world’s goods, at least the necessary share to exercise your right to live."

We believe that there is not one thing in the world which lends itself to so much abuse as money. This is not because money in itself is a bad thing. On the contrary, money is probably one of man’s most brilliant inventions, making trade flexible, favouring the sale of goods as required by needs, and making life in society easier.

But, to place money on an altar is idolatry. To make of money a living thing, which gives birth to other money, is unnatural.

Money does not breed money, as the Greek philosopher Aristotle said. Yet, how many contracts are entered into — contracts between individuals, contracts between governments and creditors, which stipulate that money must breed money, or else properties or freedoms are forfeited?

Little by little, everybody has sided behind the theory, and especially behind the practice, that money must produce interest. And in spite of all the Christian teaching to the contrary, the practice has made so much headway that, so as not to lose in the furious competition around the fertility of money, everybody must behave today as if it was natural for money to breed money. The Church has not abrogated her old laws, but it has become impossible for her to insist on their application.

The methods used to finance World War II, in which we were Churchill, Roosevelt, and Stalin’s acolytes to defend Christianity, solemnly consecrated the rule that money, even money thrown into the sea or into the burning flames of cities, must bear interest. We refer here to the Victory Bonds, which financed destruction, which did not produce anything, and which had to bear interest just the same.

So that our readers do not pass out thinking about their savings put into industry or loan institutions, let us hastily make a few distinctions.

If money cannot increase by itself, there are things that money buys which logically produce developments. Thus

I set aside $5,000 to purchase a farm, or animals, seeds, trees, machinery. With intelligent work, I will make these things produce others.

The $5,000 was an investment. By itself it has not produced anything; but thanks to this $5,000, I have been able to get things that have produced.

Let us suppose that I did not have this $5,000. But my neighbour had it, and he did not need it for a couple of weeks. He loaned it to me. I think it would be proper for me to show my gratitude by letting him have a small portion of the products which I get, thanks to the productive capital which I have thus been able to obtain.

It is my work which has made his capital profitable. But this capital itself represents accumulated work. We are then two, whose activities — gone by for him, present for me — cause some production to appear. The fact that he waited to draw on the country’s production with the money he received as a reward for his work allowed me to get the means of production that I would not have had without it.

We are therefore able to divide the fruits of this collaboration between us. There remains to determine, by agreement and equity, the part of production that is owed to the capital.

What my lender will get in this case is, strictly speaking, a dividend. (We divided the fruits of production.)

The dividend is perfectly justifiable, when production is fruitful.

* * *

This is not exactly the idea that is generally attached to the word "interest". Interest is a claim made by money, in function of time only, and independently of the results of the loan.

Here is $1,000. I invest it in federal, provincial, or municipal bonds. If I purchase bonds that bear 4% interest, I ought to get $40 in interest every year, just as truly as the earth will make one revolution around the sun during this period of time. Even if the capital is used up without any profit, I must get my $40. That is interest.

We cannot see anything that justifies this claim, save that it is customary. It does not rest upon any principle.

There is therefore justification for a dividend, because it is subordinated to production growth. There is no justification for interest in itself, because it is dissociated from realities; it is based on the erroneous idea of a natural and periodical generation of money.

In practice, he who brings his money to the bank indirectly puts it into a productive industry. The bankers are professional lenders, and the depositor passes his money to them, because they are capable of making it thrive better than he can, without having to look after it himself.

The small interest that the banker enters to the depositor’s credit from time to time, even at fixed rates, is in fact a dividend, a share from the income that the banker, with the help of the borrowers, has obtained from productive activities.

In passing, let us say a word on the morality of investments. Many people are not preoccupied in the least with the usefulness or the noxiousness of activities that their money will finance. As long as it yields profits, they say, it is good. And the more profit it yields, the better the investment is. A pagan would not reason differently.

If a house-owner does not have the right to rent his house to serve as a brothel, even though it would be very profitable, the owner of savings does not have any more right to put them into enterprises which ruin souls, even if the enterprises fill pockets.

Moreover, it would be much preferable for the backer and the entrepreneur to be less dissociated. The smaller industry of old was much more sound: The financier and the entrepreneur were the same person. The corner storekeeper is still in the same situation. The chain stores are not. The co-operative, the association of people, keeps the relation between the use of money and its owner, and has the advantage of making possible enterprises which exceed the resources of one sole individual.

Let us go back to the beginning question: Should money claim interest? We are therefore inclined to answer: Money can claim dividends when there are fruits. Otherwise, no.

If contracts are drafted differently, if the farmer must pay back interest, even though he did not receive any crop that year; if the farmers of Western Canada must honour liabilities at 7%, when the Financiers who lead the world cause prices to fall to one-third of what they were, this does not change anything about the principle. The only thing this proves is that reality has been exchanged for trickery.

But if money can claim dividends, when there is a production increase, this production increase must automatically create an increase in money. Otherwise, the dividend, while being perfectly justifiable, becomes impossible to provide without dealing a blow to the public from which it was extracted.

I was saying a few lines above: If, thanks to the $5,000 which allowed me to buy ploughing implements, I have increased my production, the lender is entitled to a share of these good results. This is very easy to do if I let him have a share of these increased products. But if it is money that I must give to him, it is quite another story. If there is no increase of money in the public, my increased production creates a problem: more offered goods, but no increase of money in step with them. I may be successful at displacing another seller, but he will be the victim.

You can tell me that the $5,000 must have contributed to increasing money in circulation. Yes, but I must pump back the $5,000, plus what I call the dividend, what others call interest.

Then the problem is not settled. And in our economic system, it cannot be. For money to increase, it is necessary that the bank — the only place where the increase is created — lends some somewhere. But in lending it, the bank exacts a repayment that is also increased. The problem snowballs.

The Social Credit system would settle that problem, as well as settle many other problems.

The dividend is a legitimate, normal, logical thing. But the present system does not allow anyone to pay it without making it hurt somewhere.

As a matter of fact, the only passage in the Gospel where it is mentioned that Jesus used force is when He drove the money changers out of the Temple with a scourge of cords, and overthrew their tables (as reported in Matthew 21:12-13 and Mark 11:15-19), precisely because they were lending money at interest.

As a matter of fact, the only passage in the Gospel where it is mentioned that Jesus used force is when He drove the money changers out of the Temple with a scourge of cords, and overthrew their tables (as reported in Matthew 21:12-13 and Mark 11:15-19), precisely because they were lending money at interest.

There was, at that time, a law that the tithes or taxes of the Temple could be paid only in one certain coin called the "half shekel of the sanctuary", of which the money changers had managed to obtain the monopoly. There were several different coins at that time, but the people had to obtain this particular coin with which to pay their Temple Tax. Moreover, the doves and the animals that the people bought for sacrifice also could only be bought with this same special coin that the money changers exchanged to the pilgrims, but at a cost of twice or more times its actual worth, when it was used to buy commodities. So Jesus overthrew their tables, and said:

"My house shall be called a house of prayer; but you have made it a den of thieves."

The Bible contains several texts that clearly condemn the lending of money at interest. Moreover, more than 300 years before Jesus Christ, the great Greek philosopher Aristotle also condemned lending at interest, pointing out that "money, being naturally barren, to make it breed money is preposterous." Furthermore, the Fathers of the Church, since the remotest times, always unequivocally denounced usury. Saint Thomas Aquinas, in his Summa Theologica (2, 2, Q. 78), thus summarized the teaching of the Church on lending money at interest:

St. Thomas Aquinas

St. Thomas Aquinas"It is written in the Book of Exodus (22, 24): `If you lend money to any of my people who are poor, that dwells with you, you shall not be hard upon them as an extortioner, nor oppress them with usury.’ He who takes usury for a loan of money acts unjustly, for he sells what does not exist, and such an action evidently constitutes an inequality and, consequently, an injustice... It follows then that it is wrong in itself to take a price (usury) for the use of money lent, and as in the case of other offenses against justice, one is bound to make restitution of his unjustly acquired money."

In reply to the text of the Gospel on the parable of the talents (Matthew 25:14-30 and Luke 19:12-27) which, at first sight, seems to justify interest ("Wicked and slothful servant... why did you not put my money into the bank, so that I might have recovered it with interest when I came?"), Saint Thomas Aquinas wrote:

"The interest mentioned in the Gospel must be taken in a figurative sense; it means the additional spiritual goods asked of us by God, who wants us to always make better use of the goods He entrusted us with, but this is for our benefit and not His."

So this text of the Gospel cannot justify interest since, as Saint Thomas says, "an argument cannot be based on figurative expressions."

Another passage of the Bible that presents difficulties is Deuteronomy 23:20-21: "You shall not demand interest from your brother on a loan of money or food or of anything else. You may demand interest from a foreigner, but not from your brother." Saint Thomas explains:

"The Jews were forbidden to take interest from `their brothers’, that is to say, from other Jews; this means that demanding interest on a loan from anyone is wrong, strictly speaking, for one must consider every man as `one’s neighbour and brother’, especially according to the evangelical law that must rule mankind. So the Psalmist, talking about the just man, says unreservedly: `he who lends not his money at usury’ (14:4) and Ezekiel (18:17): `a son who accepts no interest or usury’."

If the Jews were allowed to demand interest from a foreigner, Saint Thomas wrote, it was tolerated in order to avoid a greater evil, for fear that they might charge interest to other Jews, the worshippers of the true God. Saint Ambrose, commenting on the same text, gives to the word "foreigners" the meaning of "enemies", and concludes: "One may seek interest from the one he legitimately wants to harm, from the one whom it is lawful to wage war with."

Saint Ambrose also said: "What is usury, if not killing a man?"

Saint John Chrysostom: "Nothing is more shameful or cruel than usury."

Saint Leo: "The avarice that claims to do its neighbour a good turn while it deceives him is unjust and insolent... He who, among the other rules of a pious conduct, will not have lent his money at usury, will enjoy eternal rest... whereas he who gets richer to the detriment of others deserves, in return, eternal damnation."

In 1311, at the Council of Vienna, Pope Clement V declared null and void all secular legislation in favour of usury, and "all who fall into the error of obstinately, maintaining that the exaction of usury is not sinful, shall be punished as heretics."

Benedict XIV

Benedict XIVOn November 1, 1745, Pope Benedict XIV issued the encyclical letter Vix Pervenit, addressed to the Bishops of Italy, about contracts, and in which usury, or money-lending at interest, is clearly condemned. On July 29, 1836, Pope Gregory XVI extended this encyclical to the whole Church. It says:

"The kind of sin called usury, which lies in the loan, consists in the fact that someone, using as an excuse the loan itself — which by nature requires one to give back only as much as one has received — demands to receive more than is due to him, and consequently maintains that, besides the capital, a profit is due to him, because of the loan itself. It is for this reason that any profit of this kind that exceeds the capital is illicit and usurious.

"And in order not to bring upon oneself this infamous note, it would be useless to say that this profit is not excessive but moderate; that it is not large, but small... For the object of the law of lending is necessarily the equality between what is lent and what is given back... Consequently, if someone receives more than he lent, he is bound in commutative justice to restitution..."

In 1891, Pope Leo XIII wrote in his Encyclical Letter Rerum Novarum: "The mischief has been increased by rapacious usury, which, although more than once condemned by the Church, is nevertheless, under a different guise, but with like injustice, still practiced by covetous and grasping men. "

On this matter, it is interesting to consider the experience of the Islamic banks: the Koran — the holy book of the Moslems — forbids usury, as the Bible of the Christians does. But the Moslems took these words seriously and have set up, since 1979, a banking system that conforms with the rules of the Koran: Islamic banks charge no interest on neither current nor deposit accounts. They invest in business, and pay a share of any profits to their depositors. This is not the Social Credit system implemented in its entirety yet but, at least, it is a more than worthy attempt at putting the banking system in keeping with moral laws.

| Previous chapter - Banks create money as a debt | Next chapter - The chronic shortage of puchasing power |

Alain Pilote has been the editor of the English edition of MICHAEL for several years. Twice a year we organize a week of study of the social doctrine of the Church and its application and Mr. Pilote is the instructor during these sessions.

Rougemont Quebec Monthly Meetings

Every 4th Sunday of every month, a monthly meeting is held in Rougemont.

Subscribe

Subscribe