During the general elections of 1954 in New Zealand, eleven percent of the electors voted for Social Credit candidates, though the movement had few material means with which to wage their campaign.

This completely unexpected development sent a cold chill through the ranks of the orthodox. The government judged the situation to be serious enough to appoint a royal commission to study and report on the pros and cons of this doctrine which was winning more and more adherents.

After having been granted numerous delays, the commission finally presented its report at the beginning of April of this year, 1956.

A news despatch from Auckland (New Zealand), signed by J. C. Graham of the Canadian Press, summarized the conclusions of the commission. The despatch was printed in all the Canadian dailies on April 4 or the day following. It announces tersely:

The report of the Royal Commission on Monetary Affairs completely rejects the proposals brought forward by Social Credit for the reform of the economic system of New Zealand.

This was a foregone conclusion and only made Crediters smile. The sparrows, had passed judgment on the eagle and had found the eagle guilty. But the eagle continues to soar aloft while the sparrows continue to peck away at the dung heap.

This is not the first time, and certainly not the last that Social Credit has been considered unacceptable, its solutions to financial problems judged spurious. But the judgment has not hindered its being accepted as something both logical and humane by an ever-increasing number of people in New Zealand as well as in Australia, Canada, England and wheresoever it has been presented to the people. The very good sense it makes, more than prevails over the sententious declarations of the economists and commissions whose written conclusions have more than probably, been formulated even before their investigations got under way.

According to the news report, the commission's findings point out that the witnesses for Social Credit contradicted one another.

We have not as yet received, much less read this report of 500 pages, of which, according to Graham's report, 70 pages have been devoted to the testimony given before the members of the commission by Crediters of New Zealand.

Nevertheless, we have managed to learn something of various sections of the proffered testimony which were reproduced verbatim in the pages of the New Zealand Social Crediter; and in particular, of a long memorandum presented by Miss M. H. M. King, M. A., of Dunedin, and the long interrogation to which she was submitted. The questions were quite obviously formulated with a view to embarrassing the witness rather than as a serious attempt to learn something about the monetary proposals of Social Credit. Nonetheless, Miss King's replies were clear and intelligent and involved no contradictions whatsoever.

The principles of Social Credit were laid down in the books written by the Scottish engineer, Major C. H. Douglas, and they are the same in any country anywhere in the world. Consequently, there cannot be any contradictions between authentic exposés of the doctrine of Social Credit. Quite naturally, the withnesses under interrogation may differ in the manner in which they express themselves or in the methods proposed for the establishment of Social Credit in New Zealand.

Here in Canada we are a long way from New Zealand. But we are convinced that those who voted for Social Credit in New Zealand were dissatisfied with pretty much the same conditions which are giving rise to dissatisfaction in other countries; the disparity between the productive potential and the ability to pay, the gap between the price of products on the market and the purchasing power in the hands of the consumers.

Lack of purchasing power can be caused by something other than the small number of bills in the wallets of would-be buyers. It can result from rising prices, inflation, from the diminishning value of the dollar in Canada and the pound sterling in New Zealand.

Social Credit corrects just these two very causes of the decline of purchasing power. This, the Royal Commission does not seem to have understood even in the slightest degree. And in fact, Social Credit cannot be understood if you judge it in the light of the modern financial system.

Under the existing system any increases in money or financial credit bring about a rise in prices because they reach the public through the channel of industry only, thus creating costs which must necessarily go into prices. But Social Credit provides a channel by which these increases may go directly into the pockets of the consumer, and at the same time sets up machinery for regulating prices.

The Commission states that the evidence set forth by Social Credit does not succeed in proving that there exists a chronic disparity between purchasing power and prices.

Does the Commission need proof of a fact about which the whole community is complaining? If we had to prove disparity between purchasing power and prices we would simply bring forward all the women of this nation — and others as well — who every week go shopping with the pay cheques of their husbands. We could similarly bring forward all those who cannot go shopping because they have no money.

We would also present all the debtors, because their debts highlight the difference between the price of what they bought and the inadequate purchasing power with which they had to make the purchase. To this parade of individual witnesses we would ask to join the municipal councils, the school commissions and other public bodies, all of which are obliged to delay the public projects demanded by the community, or are forced to borrow in order to realize them, because their capacity to pay does not match their ability to execute.

The proposed solutions are outdated, says the report:

The Commission adds that Social Credit has proposed solutions which would be practical in an economic crisis like that of 1930. But no allowance has been made for the changes which have come to pass since then.

Strangely enough, during the economic crisis of the 30's, neither the government of New Zealand nor that of Canada would admit that Social Credit was the answer to the problem. And yet today they tell us that it was the solution for that time. Who's guilty of contradictions now?

Likewise, Dr. Copeland, supposed to be the final authority on economics in Australia, would not, during the 30's, so much as tolerate the mention of Social Credit. A few years later, however, he wrote that the economic crisis could have been ended by liberating financial credit.

Social Credit is not just an economic remedy to be used during times of economic crisis. It is devised to distribute the abundance of goods and such a distribution is not a matter for crises only. Social Credit removes the purely financial obstacle by making financial credit an exact reflection of real credit. And real credit is nothing more than the capacity to produce and deliver goods, when and where they are needed at the rate and in the measure required.

This harmony between real possibilities and the financial means by which these possibilities are realized, is a formula which is valid for all times and for all peoples.

The report goes on to say that the real problem in New Zealand is not a lack of money but an excess of it. How strange to hear people lamentring the fact that they have too much buying power! Would they have us believe that New Zealanders' wallets are stuffed with money but that their stores are empty?

If the citizens of New Zealand are complaining it certainly isn't because they have too many goods — no one is obliged to buy! — but it is because they are not able to pay for these goods; the prices are beyond their financial means.

Or if there are no complaints, then why the investigation? And why did eleven percent of the electors vote for Social Credit in spite of the fact that the organization lacked the customary material means for electioneering?

A curious remark of the news report runs as follows:

The report adds that the ultimate aim of Social Credit is the abolition of debt and interest and the creation of a national dividend, which could only result in the abolition of private property.

In the first place it is not true that the ultimate aim of Social Credit is the abolition of debt and interest charges. Its ultimate aim is to serve the individual in his temporal needs and to free him from the never-ending cares of the material world, so that he might the better occupy himself with other activities more in agreement with his nature.

But to us the most perplexing question is, how does the abrogation of debt and interest charges and the establishment of a national dividend contribute to the abolition of private property? Can one not be a property owner without having to contract debts? and pay interest charges? And does receiving a dividend disqualify one for ownership of property? Are capitalists any the less proprietors because they collect dividends?

It would have been a simple matter to have foretold the tenor of the Royal Commission's report. When the norms of judgment are based on the principles of present day finance, how can the judgment be favorable to propositions opposed to this finance? Furthermore, the Commission was decreed and its members appointed by a government alarmed by a movement whose growth was such that it could enter candidates in the electoral campaign. Are we to imagine that the Commission was set up to report favorably on this movement? Wasn't it rather a matter of finding some way of containing the organization's growth? If such was the plan of the party in power then it misfired in spite of the report and the fanfare of publicity given it.

Only some twelve years ago the Canadian Social Science Research Council accepted from the Rockefeller Institute a very generous grant — running into the millions — for the purpose of studying the antecedents and the growth of the Social Credit movement in Alberta. Was the Rockefeller Institute genuinely concerned in justifying the Social Credit movement? Did it really hope that it might find in Social Credit a means of placing finance at the service of individuals, all individuals? A likely supposition, indeed! Serving the people is the last consideration of those administering the millions acquired through the exploitation of the people.

The enquiry was entrusted to a group of university professors; it is hardly likely that they would arrive at conclusions condemning the very system they were teaching. The findings were published in a series of volumes. In the fourth volume the doctrine of Douglas was attacked, his teachings being twisted in order to render them vulnerable.

This criticism was authored by C. B. Macpherson, a professor of political economy at the University of Toronto and holder of a diploma from the university of London. Macpherson was only able to repeat arguments which had already been set forth by Gaitskell (present leader of the Socialist party in England), Cole, Hiskee, Franklin, Lewis and Copeland, and aptly refuted by Douglas.

These economists, bravely flying their degrees, drive themselves almost to distraction trying to prove to us that production automatically puts into circulation all the purchasing power necessary to buy the fruits of production. This theory is so ridiculously at variance with the experience of the people, who must go through the daily routine of life, that the reports of these gentlemen in the mortar boards have ended up gathering dust on some out-of-the-way shelf in the library. As for Social Credit, its growth and influence is ten times what they were a decade ago. Common sense prevails.

Rougemont Quebec Monthly Meetings

Every 4th Sunday of every month, a monthly meeting is held in Rougemont.

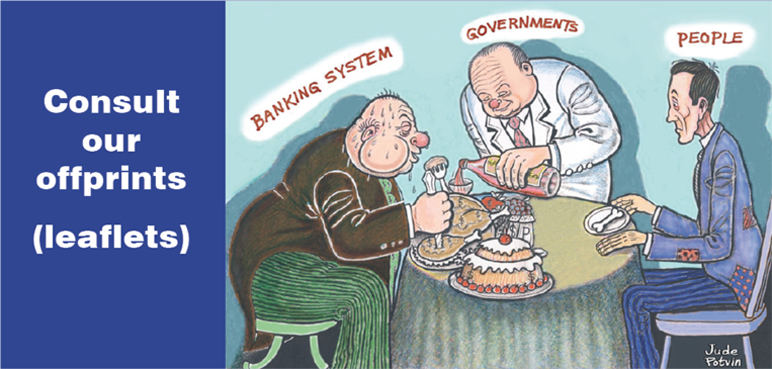

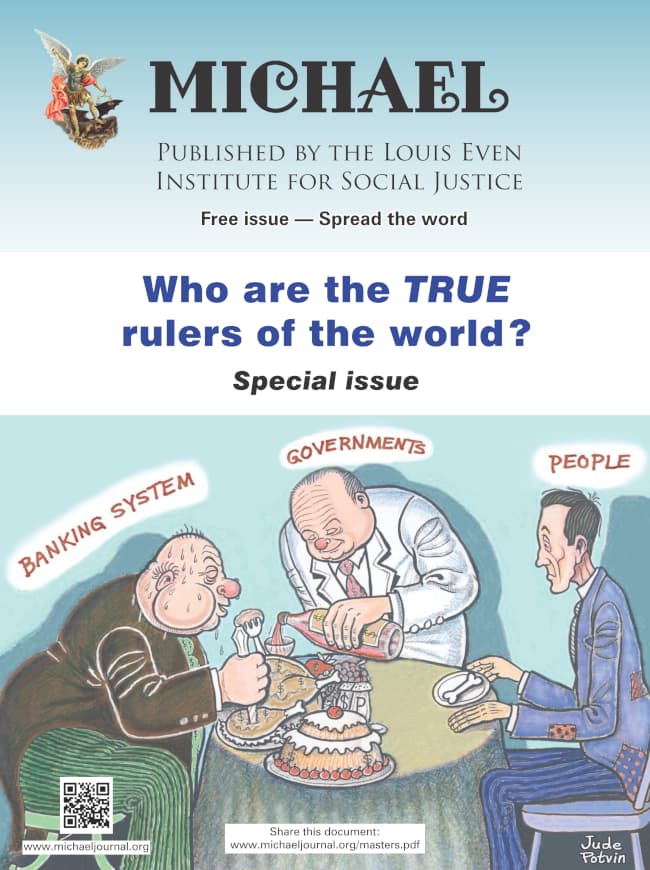

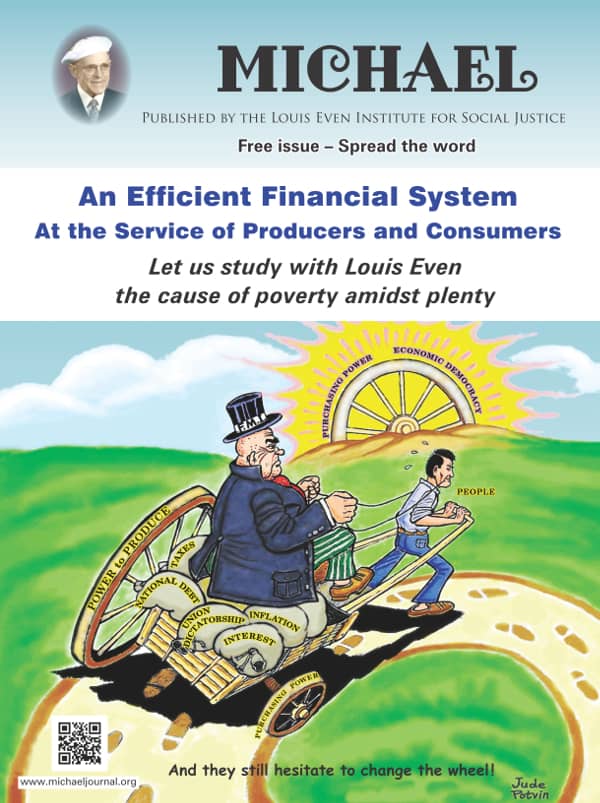

In this special issue of the journal, MICHAEL, the reader will discover who are the true rulers of the world. We discuss that the current monetary system is a mechanism to control populations. The reader will come to understand that "crises" are created and that when governments attempt to get out of the grip of financial tyranny wars are waged.

In this special issue of the journal, MICHAEL, the reader will discover who are the true rulers of the world. We discuss that the current monetary system is a mechanism to control populations. The reader will come to understand that "crises" are created and that when governments attempt to get out of the grip of financial tyranny wars are waged. An Efficient Financial System, written by Louis Even, is for the reader who has some understanding of the Douglas Social Credit monetary reform principles. Technical aspects and applications are discussed in short chapters dedicated to the three propositions, how equilibrium between prices and purchasing power can be achieved, the financing of private and public production, how a Social Dividend would be financed, and, finally, what would become of taxes under a Douglas Social Credit economy. Study this publication to better grasp the practical application of Douglas' work.

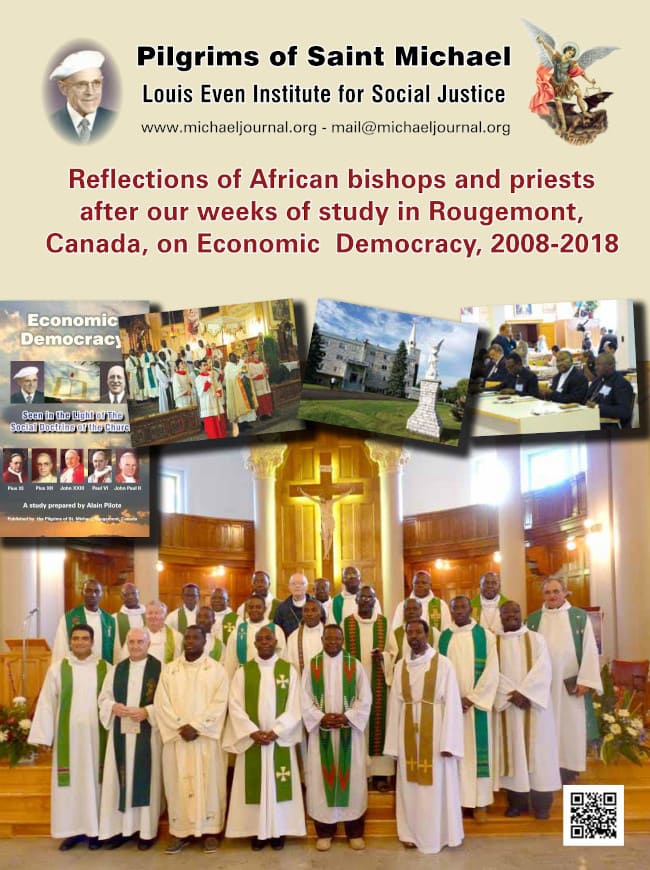

An Efficient Financial System, written by Louis Even, is for the reader who has some understanding of the Douglas Social Credit monetary reform principles. Technical aspects and applications are discussed in short chapters dedicated to the three propositions, how equilibrium between prices and purchasing power can be achieved, the financing of private and public production, how a Social Dividend would be financed, and, finally, what would become of taxes under a Douglas Social Credit economy. Study this publication to better grasp the practical application of Douglas' work.  Reflections of African bishops and priests after our weeks of study in Rougemont, Canada, on Economic Democracy, 2008-2018

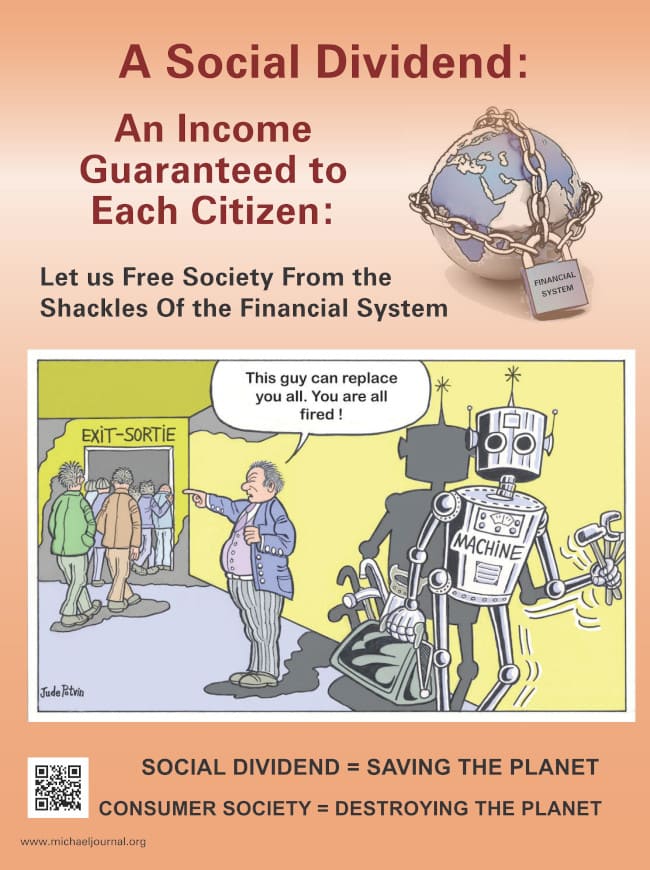

Reflections of African bishops and priests after our weeks of study in Rougemont, Canada, on Economic Democracy, 2008-2018 The Social Dividend is one of three principles that comprise the Social Credit monetary reform which is the topic of this booklet. The Social Dividend is an income granted to each citizen from cradle to grave, with- out condition, regardless of employment status.

The Social Dividend is one of three principles that comprise the Social Credit monetary reform which is the topic of this booklet. The Social Dividend is an income granted to each citizen from cradle to grave, with- out condition, regardless of employment status. Economic Democracy is a book to explain Social Credit in lessons presented in logical order so it may be easier to the reader to grab the main principles of Social Credit rapidly and somehow easily.

Economic Democracy is a book to explain Social Credit in lessons presented in logical order so it may be easier to the reader to grab the main principles of Social Credit rapidly and somehow easily. In This Age of Plenty deals with Social Credit, but it does not exhaust the topic. Social Credit principles address social and political matters, as well as, or even more so, than economics and will put civilization on a new course.

In This Age of Plenty deals with Social Credit, but it does not exhaust the topic. Social Credit principles address social and political matters, as well as, or even more so, than economics and will put civilization on a new course. From Debt to Prosperity outlines briefly the economic analysis and constructive proposals known as Social Credit.

From Debt to Prosperity outlines briefly the economic analysis and constructive proposals known as Social Credit.

Subscribe

Subscribe