Last month we examined the creation of financial credit (money), and cited a number of leading banking authorities to confirm the fact that banks, with pen and ink, actually create "money". Because we have been conditioned to think in terms of dollars instead of things, and order our society according to financial limitations rather than physical realities, it is well that we have a clear understanding of "money" before continuing our study.

Let us examine some further evidence on our banking system — evidence from a most authentic source. (The following summary of evidence, most of it verbatim, was originally compiled by H. E. M. Kensit of Ottawa.)

The Federal Government maintains a Standing Committee on Banking and Commerce. During the 1939 Session this Committee confined its proceedings to an examination respecting the Bank of Canada. The witness for the Bank, subject to cross-examination, was Mr. Graham F. Towers, its Governor. Mr. Towers made a good witness — while immovable as to a direct "yes" or "no" where such answer would not be correct without qualification, he gave frank and definite answers to many questions. The Committee held thirty sittings and its Proceedings cover 850 pages, so that to bring out the important points necessitates drastic condensation. We have endeavoured to do this fairly and in each case we give the page number of the Proceedings so that reference can be made for the context, and for minor qualifications if there be such.

Bear in mind that the following statements made or agreed by Mr. Towers are those of the Governor of a government owned central bank, To make the following matter clear we divide it under suitable headings:

(The following extracts are from the Minutes of Proceedings and Evidence Respecting the Bank of Canada, Committee on Banking and Commerce, 1939. Government Printing Bureau, Ottawa.)

MR. TOWERS: "A government can find money in three ways: by taxation, or they might find it by borrowing the savings of the people, or they might find it by action which is allied with an expansive monetary policy, that is borrowing which creates additional money in the process." (P. 29.)

Q: A banker can purchase a federal government bond by accepting from the government, we will say a bond for $1,000 and giving to the government a deposit in the bank for $1,000?

MR. TOWERS: Yes.

Q: ...what the government receives is a credit entry in the banker's book showing the banker as a debtor to the government to the extent of $1,000?

MR. TOWERS: Yes.

Q: And in law all that the bank has to hold in the way of cash to issue that deposit liability is 5 per cent?

MR. TOWERS: Yes. (P. 76.)

Q: Ninety-five per cent of all our volume of business is being done with what we call exchange of bank deposits — that is simply bookkeeping entries in banks against which people write cheques?

MR. TOWERS: I think that is a fair statement. (P. 223.)

Q: ...the need of a currency gold reserve was today largely psychological so far as domestic currency was concerned?

MR. TOWERS: As far as domestic currency was concerned; yes.

Q: Then I take it that you would agree — the findings of the British MacMillan Committee, sec. 148, as follows:

"...it is not necessary that the volume of note issues should continue to be regulated, as it is now, by reference to the amount of gold held in reserve. If... the principle is adopted that gold reserves should be held, not primarily against note issues, but to meet temporary deficiencies in the balance of international payments, there need be no obstacle to the creation of a much increased volume of purchasing power without any increase in the supply of monetary gold."

And since then there has been plenty of evidence that the theory has not been worked out but is being more generally adopted as time goes on?

MR. TOWERS: Yes. (P. 277.)

Q: Now, on page 112 of the MacMillan report — we find the following:

"The sole use of gold reserve is, therefore, to enable a country to meet deficits in its international balance of payments, until the appropriate measures can be taken to bring it again into equilibrium..."

And it could be done under the administration we have, and the attitude of our governments, without weakening our internal currency system?

MR. TOWERS: Assuming that the need for expansion was a justifiable one, I would hope and expect that would be the case, yes. (P. 278.)

Q: ...having the huge available money resources which we are neither using nor abusing, the elimination of our gold reserve provision in our Bank of Canada Act would not alter the policy of the Bank of Canada or the government at all?

MR. TOWERS: No; in other words, that gold reserve provision is in no sense a hampering one and I would not expect it to be in the visible future.

Q: And if we eliminated that from our Bank of Canada Act, the gold provision of 25% as against Bank of Canada note issues, it would not affect the monetary policy or the monetary situation in Canada at all?

MR. TOWERS: It should not, no. (P. 279.)

Q: ...the findings of the MacMillan Committee — in other words, they made a finding that the volume of purchasing power to be issued through the banking system was not necessarily to be limited by the supplies of gold; and I think we are in general agreement on that?

MR. TOWERS: Yes.

Q: But if the issue of currency and money is a high prerogative of government, then that high prerogative has been transferred to the extent of 88 per cent from the government to the merchant banking system?

MR. TOWERS: Yes. (P. 286.)

Q: When a $1,000,000 worth of bonds is presented (by the government) to the bank a million dollars of new money or the equivalent is created?

MR. TOWERS: Yes.

Q: It is a fact that a million dollars of new money is created?

MR. TOWERS: That is right. (P. 238.)

Q: Now, as a matter of fact today our gold is purchased by the Bank of Canada with notes which it issues — not redeemable in gold in effect using printing press money.... to purchase gold?

MR. TOWERS: That is the practice all over the world... (P. 283.)

Q: When you allow the merchant banking system to issue bank deposits — with the practice of using cheques you virtually allow the banks to issue an effective substitute for money, do you not?

MR. TOWERS: The bank deposits are actually, money in that sense...

Q:...as a matter of fact they are not actual money but credit, bookkeeping accounts, which are used as a substitute for money?

MR. TOWERS: Yes.

Q: Then we authorize the banks to issue a substitute for money?

MR. TOWERS: Yes, I think that is a very fair statement of banking. (P. 285.)

Q: Will you tell me why a government with power to create money should give that power away to a private monopoly and then borrow that which parliament can create itself, back at interest, to the point of national bankruptcy?

MR. TOWERS: ...we realize of course that the amount which is paid provides part of the operating costs of the banks and some interest on deposits. Now, if parliament wants to change the form of operating the banking system, then certainly that is within the power of parliament. (P. 394.)

MR. TOWERS: The banks cannot, of course, loan the money of their depositors. What the banks have done is to make loans and investments which result in a certain sum total of deposits in respect to savings that amount is $1,600,000,000 odd. Now what the depositors do with these savings is something quite beyond the control of the banks. (P. 455.)

Q: You have agreed that banks do create money:

MR. TOWERS: They, by their activities in making loans and investments create liabilities for themselves. They create liabilities in the form of deposits.'

Q: You will agree with the statement that has been made that banks lend by creating the means of payment:

MR. TOWERS: Yes, I think that is right. (P. 456.)

Q: So that with the increase of 500 million of bank deposit money (from 1934 to 1938) we have not had any inflationary result?

MR. TOWERS: We have not. The circumstances of the time have not encouraged it. (P. 643.)

Q: ...so far as war is concerned, to defend the integrity of the nation there will be no difficulty in raising the means of financing whatever those requirements may be?

MR. TOWERS: The limit of the possibilities depends on men and materials.

Q: ...and where you have an abundance of men and materials you have no difficulty, under our present banking system, in putting forth the medium of exchange that is necessary to put the men and materials to work in defence of the realm?

MR. TOWERS: That is right.

Q: Well, then, why is it, where we have a problem of internal deterioration, that we cannot use the same technique... in any event you will agree with me on this, that so long as the investment of public funds is confined to something that improves the economic life of the nation, that will not of itself produce inflationary conditions?

MR. TOWERS: Yes, I agree with that, but I shall make one further qualification, that the investments thus made shall be at least as productive as some alternative uses to which the money would otherwise have been put. (P. 649.)

Q: Would you admit that anything physically possible and desirable can be made financially possible?

MR. TOWERS: Certainly. (P. 771.)

(To be continued)

Rougemont Quebec Monthly Meetings

Every 4th Sunday of every month, a monthly meeting is held in Rougemont.

In this special issue of the journal, MICHAEL, the reader will discover who are the true rulers of the world. We discuss that the current monetary system is a mechanism to control populations. The reader will come to understand that "crises" are created and that when governments attempt to get out of the grip of financial tyranny wars are waged.

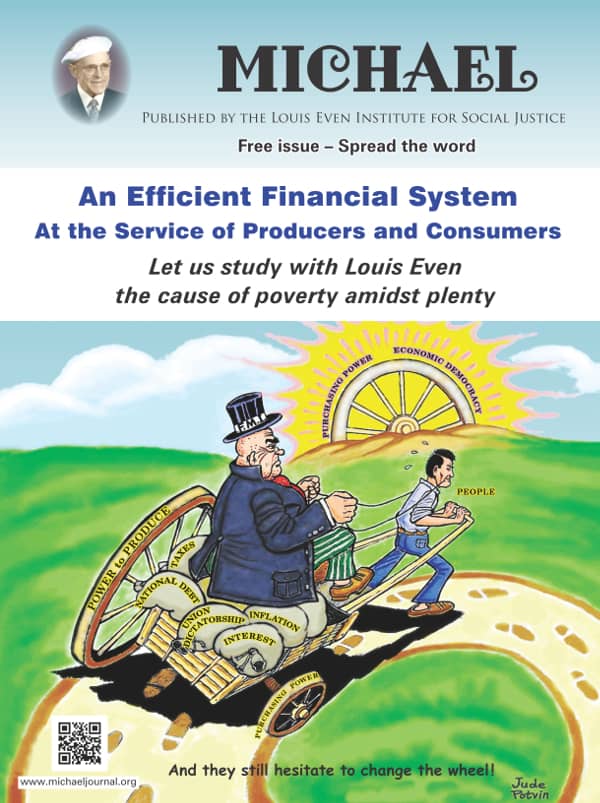

In this special issue of the journal, MICHAEL, the reader will discover who are the true rulers of the world. We discuss that the current monetary system is a mechanism to control populations. The reader will come to understand that "crises" are created and that when governments attempt to get out of the grip of financial tyranny wars are waged. An Efficient Financial System, written by Louis Even, is for the reader who has some understanding of the Douglas Social Credit monetary reform principles. Technical aspects and applications are discussed in short chapters dedicated to the three propositions, how equilibrium between prices and purchasing power can be achieved, the financing of private and public production, how a Social Dividend would be financed, and, finally, what would become of taxes under a Douglas Social Credit economy. Study this publication to better grasp the practical application of Douglas' work.

An Efficient Financial System, written by Louis Even, is for the reader who has some understanding of the Douglas Social Credit monetary reform principles. Technical aspects and applications are discussed in short chapters dedicated to the three propositions, how equilibrium between prices and purchasing power can be achieved, the financing of private and public production, how a Social Dividend would be financed, and, finally, what would become of taxes under a Douglas Social Credit economy. Study this publication to better grasp the practical application of Douglas' work.  Reflections of African bishops and priests after our weeks of study in Rougemont, Canada, on Economic Democracy, 2008-2018

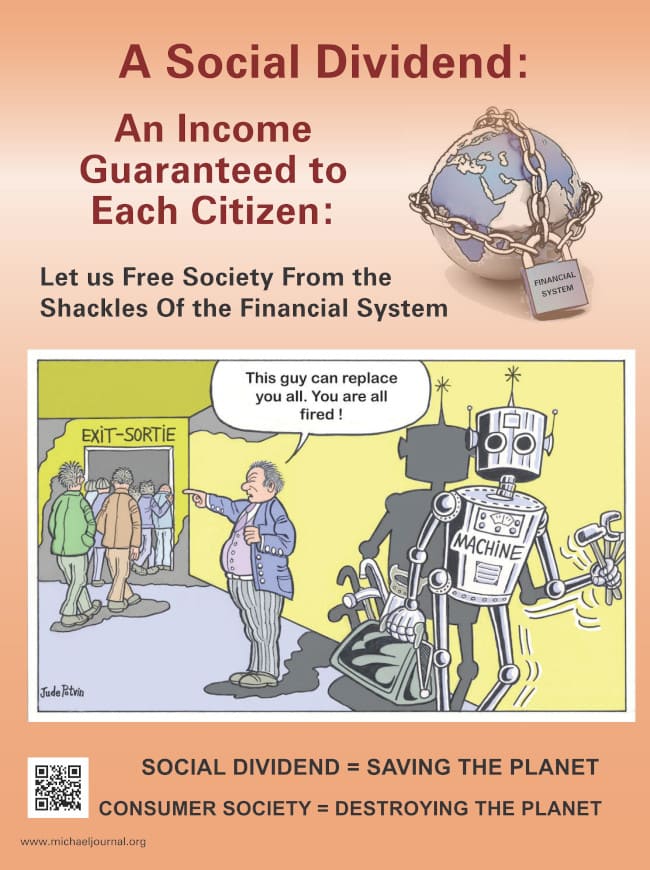

Reflections of African bishops and priests after our weeks of study in Rougemont, Canada, on Economic Democracy, 2008-2018 The Social Dividend is one of three principles that comprise the Social Credit monetary reform which is the topic of this booklet. The Social Dividend is an income granted to each citizen from cradle to grave, with- out condition, regardless of employment status.

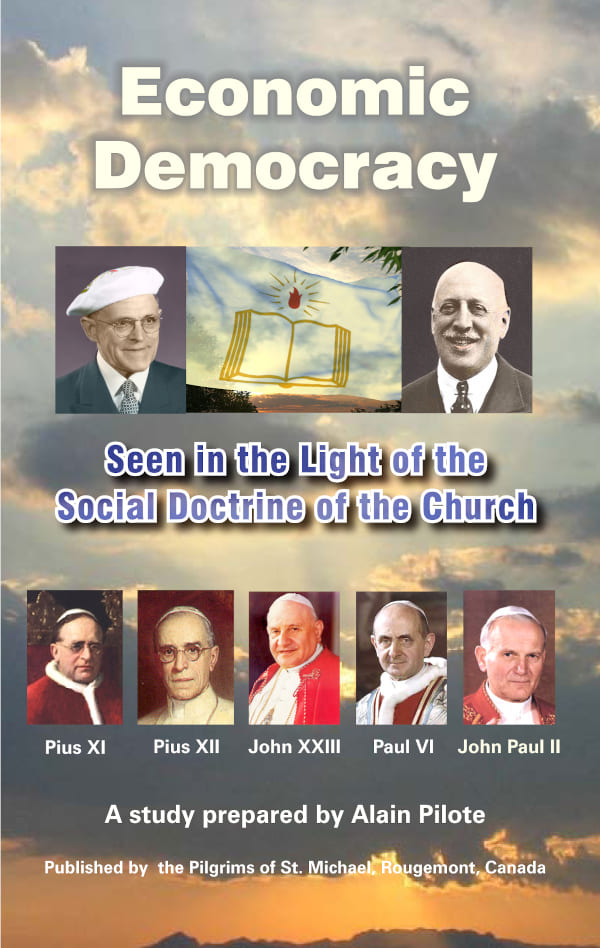

The Social Dividend is one of three principles that comprise the Social Credit monetary reform which is the topic of this booklet. The Social Dividend is an income granted to each citizen from cradle to grave, with- out condition, regardless of employment status. Economic Democracy is a book to explain Social Credit in lessons presented in logical order so it may be easier to the reader to grab the main principles of Social Credit rapidly and somehow easily.

Economic Democracy is a book to explain Social Credit in lessons presented in logical order so it may be easier to the reader to grab the main principles of Social Credit rapidly and somehow easily. In This Age of Plenty deals with Social Credit, but it does not exhaust the topic. Social Credit principles address social and political matters, as well as, or even more so, than economics and will put civilization on a new course.

In This Age of Plenty deals with Social Credit, but it does not exhaust the topic. Social Credit principles address social and political matters, as well as, or even more so, than economics and will put civilization on a new course. From Debt to Prosperity outlines briefly the economic analysis and constructive proposals known as Social Credit.

From Debt to Prosperity outlines briefly the economic analysis and constructive proposals known as Social Credit. Subscribe

Subscribe