We have in recent issues examined the development of our modern power-driven productive machine, and noted that the distributive system (finance) has failed to keep pace with the productive machine, with the result that modern society has been periodically subjected to poverty amidst abundance, inflation and deflation, and evermounting debt and taxation.

Last month we traced the evolution of money, and discussed the three kinds of money: coins, bills, and deposit currency or credit. And we noted that the government creates the former two (coins and bills), which constitute less than 10 percent of our total money, for the banks; but that the private banking system itself today exercises the prerogative of creating deposit currency or credit (cheque-book money), which constitutes some 90 percent of total money.

We continue now with an examination of the creation of money.

It should be noted that although the government creates coins and bills, it is not the practise to spend this into circulation, but rather to supply it to the private banks in exchange for gold or certain securities.

We are not on the gold standard today. But even when we were, for each dollar's worth of gold a private bank deposited with the government (Bank of Canada), the government gave in return four dollars of "cash" money — bills, etc. And for each dollar of this "cash" money the bank held, it was permitted to loan into circulation nineteen dollars of "credit money." This made the following expansion: One dollar in gold or securities expanded to four dollars in "cash" money; and this four dollars in "cash" money expanded by law nineteen times, which made 76 dollars in credit money" which the banks could create and loan. Thus the expansion on the first dollar was: 1 plus (4 x 19), which is 80 dollars — an expansion of 80 to 1. In other words, behind every dollar under the old "gold" standard, by law there stood only a little over one cent in gold or its equivalent. Actually, banking practise kept the ratio down to 30 or 40 to 1 – still a pretty elastic gold standard.

(This information is found in the evidence of the Standing Committee on Banking & Commerce, 1939, page 7 of Dr. Clark's evidence, Pages 102-3 of Graham Towers'.)

Thus do we see how the government (central government bank) creates the coins and bills for the banking system, and then the banking system expands a great inverted pyramid of financial credit (actually money, to all intents and purposes) on this tiny base. Let us examine the exact procedure by which this financial credit or cheque-book money is created and put into circulation. We shall now examine the birth of a thousand dollars of this money.

(A farmer walks into his local bank)

Mr. Banker: Good morning, Mr. Farmer. Nice morning! And what can I do for you?

Mr. Farmer: Well, I'd like to borrow a thousand dollars to put my crop in.

Mr. Banker: Yes — Well, now, what security have you got — what collateral?

(It should be noted that the banker does not go to his vault to find out what gold, securities or cash the bank has. He is interested in the security the farmer possesses.)

Mr. Farmer: Well, sir, I have a hundred acres clear, 30 head of Jerseys, 15 hogs and a herd of goats (whatever you do, don't include your wife and children — they're no 'asset' in this situation!)

Mr. Banker: Well, you have good security. I think we can look after your requirements and loan you a thousand dollars.

The banker now opens his ledger and writes the farmer's name across the top of one of the pages, and over in the right-hand credit column he credits him (by simply writing in the figures) with $950. He deducted the interest before making the loan. Now the banker hands him an account book and a cheque book — and he now has on deposit, against which he may write cheques, $950. This is brand new money just created by the banker. It did not exist five minutes earlier, when the farmer entered the bank. And it was not taken out of anyone else's account – they still have their deposits in full.

Of course, if the farmer wanted a few dollars in cash, the bank has a reserve for this purpose. But experience shows that cash makes up no more than 10 percent of the money with which business is transacted, the other 90 percent being done by financial credit instruments (cheques, drafts, etc.).

Now you have your account of $950. in the bank (new figures in their ledger), and you have a book full of cheques. You go out and make your purchases and pay your bills by issuing cheques. These cheques go back to the bank and are debited to your account. When you issue cheques equal to your original loan, your account is cancelled out.

The cost of this whole transaction to the bank was a pen, a little ink and bookkeeping. But you now owe the bank one thousand dollars.

A loan to a business or corporation involves precisely the same principles and procedure.

When a bank buys government bonds, it does so by creating the credit or money against the government's (country's) own security. It costs the bank little or nothing to buy and acquire interest-bearing bonds.

Two points should be noted:

(1) Whether the borrower be a farmer, a business, or a government, it is the borrower who puts up the security against which the money is created and loaned — not the bank. The bank merely creates the figures to monetize the borrower's real wealth or credit. The borrower borrows his own credit.

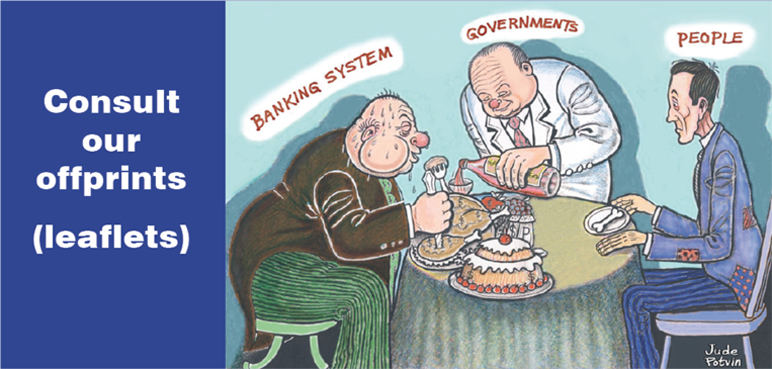

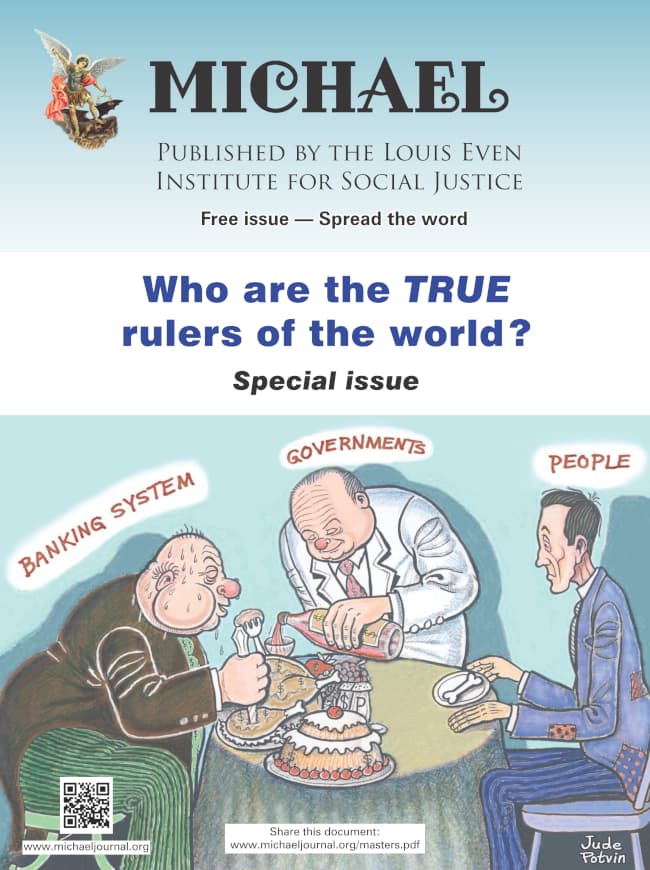

(2) Had the farmer entered the same bank, with the same collateral, in 1933 instead of 1955, he wouldn't have got the loan. In other words, the creation of money and credit, and its expansion and contraction, are controlled not by the people or parliament, but by a private monopoly. Our medium of exchange, in other words is determined not by the needs of production and consumption, but by the 'policy' of a financial monopoly. This is no reflection upon the many excellent services performed by our network of banks, so necessary in our complex society today; but it is a warning of the danger inherent in allowing the right to create and control credit and money to rest with a monopoly answerable to neither the requirements of society nor the parliament of the nation.

We shall continue this examination in coming issues.

Rougemont Quebec Monthly Meetings

Every 4th Sunday of every month, a monthly meeting is held in Rougemont.

In this special issue of the journal, MICHAEL, the reader will discover who are the true rulers of the world. We discuss that the current monetary system is a mechanism to control populations. The reader will come to understand that "crises" are created and that when governments attempt to get out of the grip of financial tyranny wars are waged.

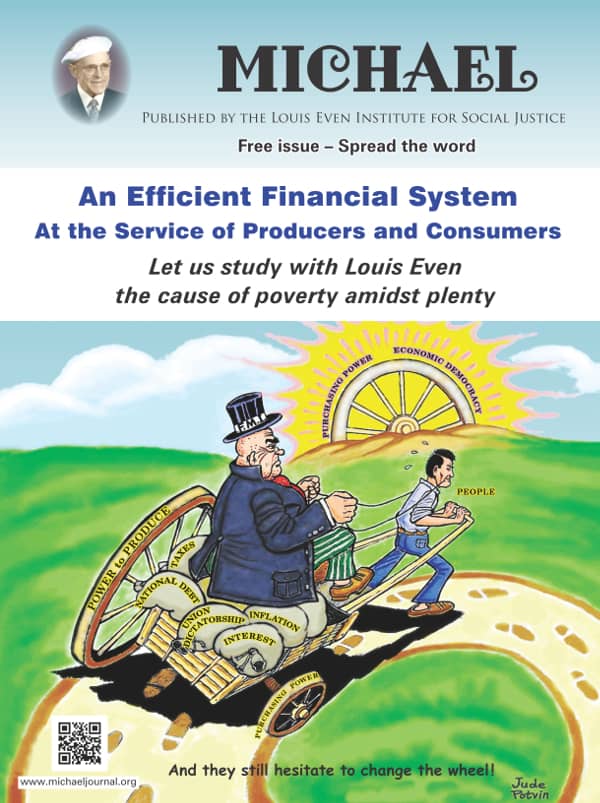

In this special issue of the journal, MICHAEL, the reader will discover who are the true rulers of the world. We discuss that the current monetary system is a mechanism to control populations. The reader will come to understand that "crises" are created and that when governments attempt to get out of the grip of financial tyranny wars are waged. An Efficient Financial System, written by Louis Even, is for the reader who has some understanding of the Douglas Social Credit monetary reform principles. Technical aspects and applications are discussed in short chapters dedicated to the three propositions, how equilibrium between prices and purchasing power can be achieved, the financing of private and public production, how a Social Dividend would be financed, and, finally, what would become of taxes under a Douglas Social Credit economy. Study this publication to better grasp the practical application of Douglas' work.

An Efficient Financial System, written by Louis Even, is for the reader who has some understanding of the Douglas Social Credit monetary reform principles. Technical aspects and applications are discussed in short chapters dedicated to the three propositions, how equilibrium between prices and purchasing power can be achieved, the financing of private and public production, how a Social Dividend would be financed, and, finally, what would become of taxes under a Douglas Social Credit economy. Study this publication to better grasp the practical application of Douglas' work.  Reflections of African bishops and priests after our weeks of study in Rougemont, Canada, on Economic Democracy, 2008-2018

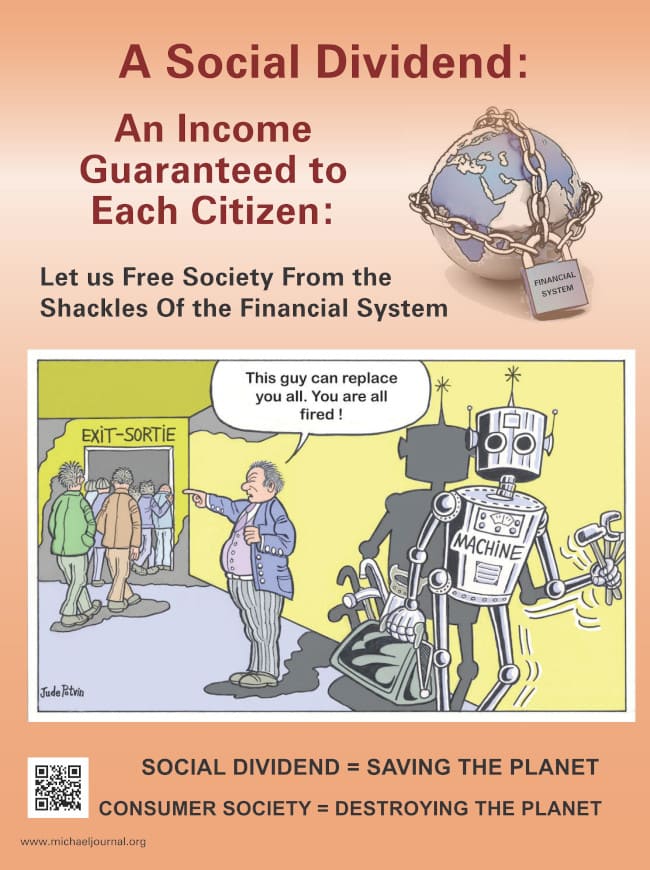

Reflections of African bishops and priests after our weeks of study in Rougemont, Canada, on Economic Democracy, 2008-2018 The Social Dividend is one of three principles that comprise the Social Credit monetary reform which is the topic of this booklet. The Social Dividend is an income granted to each citizen from cradle to grave, with- out condition, regardless of employment status.

The Social Dividend is one of three principles that comprise the Social Credit monetary reform which is the topic of this booklet. The Social Dividend is an income granted to each citizen from cradle to grave, with- out condition, regardless of employment status. Economic Democracy is a book to explain Social Credit in lessons presented in logical order so it may be easier to the reader to grab the main principles of Social Credit rapidly and somehow easily.

Economic Democracy is a book to explain Social Credit in lessons presented in logical order so it may be easier to the reader to grab the main principles of Social Credit rapidly and somehow easily. In This Age of Plenty deals with Social Credit, but it does not exhaust the topic. Social Credit principles address social and political matters, as well as, or even more so, than economics and will put civilization on a new course.

In This Age of Plenty deals with Social Credit, but it does not exhaust the topic. Social Credit principles address social and political matters, as well as, or even more so, than economics and will put civilization on a new course. From Debt to Prosperity outlines briefly the economic analysis and constructive proposals known as Social Credit.

From Debt to Prosperity outlines briefly the economic analysis and constructive proposals known as Social Credit. Subscribe

Subscribe