Financially, the province of New Brunswick is getting into water over its head, and unless something is done to rescue it soon, it might very well go under and disappear as a political entity on the Canadian scene.

Reporting to the Royal Commission on banking and finance, the New Brunswick government admitted that its situation, financially and economically, is becoming desperate. Its expenditures are rising (pushed up by costly state hospital insurance) while the base of its taxation is becoming restricted to a point where new taxation is virtually impossible.

This, the government says, leaves it with no alternative but to turn to new borrowing. Naturally borrowing costs will go up, further strain will be placed upon existing revenues and eventually a "saturation limit" will be reached in borrowing. The province will be literally unable to borrow another cent. When this happens public services and other functions will be cut back and restricted.

The government of New Brunswick goes so far as to state that unless some long-term solution is found to improve the provincial economy, there will result "... continual retardation leading to the economic and cultural disappearance of the province as a part of Canada". It will probably also mean its disappearance as a political unit in the dominion. One has only to cast the memory back to the days when Newfoundland was a ward of the British government, a political "minor" unable to exercise free will in regard to its political and economic life.

The government, in its report to the royal commission, could only ask, in sum, that it should be exempted from any policy of credit restriction; that it be made easier for the province to acquire loans from the chartered banks, during tight-money periods.

There can be no question about poverty in the province of New Brunswick. The citizens are desperately poor. Consequently, the government is poor.

The publications of the Union of Electors, Vers Demain and The Union of Electors, have carried numerous articles and photographs illustrating this poverty of the New Brunswick families. The case files of our office are filled with the names and addresses of hundreds of families which are hard put to find food and clothing for their children. The Union of Electors has on occasions carried out campaigns to gather food and clothing from its members for distribution among these poverty-stricken people of this maritime province.

In the April, 1962, issue of The Union of Electors, we carried a photograph of a page of the New Brunswick paper, L'Évangéline, on which were listed over a thousand names of families whose houses were up for sale because of non-payment of taxes. Obviously, these people were too poor to pay the property tax.

Our March issue of this year carried another article on poverty in New Brunswick in which article we published a letter from a father about to be evicted with his family for non-payment of taxes. When you stop to consider each particular case of such evictions, and try to realize the heartbreak and the torture of anxiety and worry through which these families must pass, the tragedy of such poverty as we witness in New Brunswick becomes all too apparent.

In December of 1960, Mr. Paul Lordon, who was at that time a Liberal M.P. to the provincial house of N.B., struck out hard against the tax collection system of New Brunswick. How, said he, could you possibly expect to collect taxes from people, a people, who had no money.

"In any consideration of the difficulty of collecting taxes in the county, it is important to discover whether such difficulty arises from the fault of the tax collection system on the one hand, or the inability of the people to pay on the other... If the people cannot pay then there is no point in changing the system of tax collection because no system of tax collection is going to work. To put it in common everyday language, you cannot take blood out of a stone."

Mr. Lordon realized one very important aspect of the New Brunswick financial situation which seems to have escaped most of the authorities: the people have no money with which to pay taxes!

Another man who did not hesitate to paint the picture in its true colours was J.C. Van Horne, ex-MP. to the federal parliament from the constituency of Restigouche-Madawaska in New Brunswick. Mr. Van Horne, was known as the "enfant terrible" of the federal house because he was so plainspoken and so ready to speak even if it meant tearing into his own party and his own chief. And one of Mr. Van Horne's favorite topics was the poverty of his people. Speaking before the House in February of 1960, he pleaded for aid for his poverty stricken province.

"I ask the government to give the people of my riding a half-decent break and to do it now. If something is not done within the next month children will again be going to school without breakfast and some of them will be fainting in school because they have had nothing to eat."

Mr. Van Horne felt that he knew where part of the trouble lay. Said he:

"In my opinion tight money is one of the main causes of unemployment in this country today... Another thing I do not like about our system here is the Bank of Canada. The Bank of Canada in my opinion is more than partly responsible for the unemployment situation we have today... We should make money available to our provincial governments, our municipalities and our institutions interest-free or with low interest rates or even with interest rates subsidized by the government."

These two men, elected representatives of the people, knew the grim story of New Brunswick's poverty from first-hand experience. They were men whose consciences would not permit them to be silent. So they told the parliaments of the people and the world in general. The great tragedy of their effort is that there have been few if any other voices to strengthen their protest.

The government of New Brunswick might well tell its tragic story to the Royal Commission, appealing against the economic and political death which is threatening it. For with the people becoming poorer and poorer, the orthodox methods commonly used by governments of all sorts to raise money - namely, taxation — are being denied to the N.B. government. And this government recognizes that fact.

What, then, is the solution? By what means is the government of New Brunswick to save itself?

One means set down in the brief to the Royal Commission, was that of borrowing. With the base of taxation being steadily restricted, increasing reliance must be placed on borrowing, says the brief.

But borrowing is nothing other than delayed taxation. Even supposing that the government were able to borrow at normal rates of interest; even supposing that it were able to develop or revive what industries it has, through borrowing, what else will the government have achieved except to plunge its people deeply into debt to the banks, burdening them with a debt load which will strangle their efforts to struggle to a better standard of living, not only in this generation, but in generations to come. Borrowing benefits no one but the banker and the financier. It gives finance a strangle-hold on the economy, which, though it might be developed, benefits no one but the lender.

The solution proposed by Social Credit is for the community to exploit its natural resources for itself. The resources belong to the people. They are exploited by the people. Therefore the people should enjoy the fruits of such exploitation,

In the May, 1961, issue of The Union of Electors, we ran an article by Mr. Louis Even, Director-General of our movement and Editor-in-chief of Vers Demain, in which he lays down the framework for a system which will enable provinces to exploit their own benefit. Calling for the institution of a provincial credit system, Mr. Even envisages the setting up of a provincial organism which might, in this case, be called, New Brunswick Credit (much in the same fashion as we speak of, for example, Quebec Hydro, or Ontario Hydro).

"Legislation is passed (we are here quoting directly from the article with the necessary changes to make it apply to New Brunswick) establishing a credit commission which will be known as New Brunswick Credit. To benefit completely from this organization, the population of the province is invited to make use of N.B. Credit in all the payments it may make within the province. This will be effected through credit accounts in the books of the different branches of N.B. Credit.

"To participate in N.B. Credit, all that is necessary is to deposit at a branch of N.B. Credit, a sum of money — money issued by the banking system. Such an amount will be inscribed to the credit of the depositor, just as is done in ordinary banks.

"The bank credit thus deposited will be used to make payments outside the province. For all payments either within or outside the province, the individual having an account with N.B. Credit will simply sign a "transfer of credit", indicating the amount to be transferred — just as is done in ordinary banks. The branch of N.B. Credit, within which such a transfer is made, goes about completing the transfer as indicated. If the payment is sent outside the province, N.B. Credit will make the payment in banking money drawn from the total of deposits made by the depositors; evidently, the total of the provincial credit in the books of N.B. Credit will have been decreased by that amount.

"It is not difficult to understand that if the people use as little as possible of the banking money which they obtain from some source or other, no difficulty will arise in making payments outside the country as long as the people do not get most of their products from outside the province, making little use of the supply of products inside the province.

"It is much in this fashion that trade between countries takes place. The Japanese who send us products are not paid in Canadian money but in Japanese money; and vice versa. The whole business of financing such trade is carried on without difficulty in the offices of the financiers. With the regard to the setup which we have proposed for N.B., these outside payments would automatically be regulated in the offices of N.B. Credit.

"The advantage of such an institution is that there is no financial obstacle hindering the people of the province from making use of their manpower and natural resources so that they may produce all the goods they require to meet their needs and demands.

"Thus, all which is physically possible in New Brunswick for filling needs both private and public will be made financially possible through the accounting service of New Brunswick Credit.

"Would such an organization be contrary to the Constitution? — Not at all. There would be no issuance of money, either metal, paper or in the form of banking credit. It would be a simple and direct use of the credit of the province of New Brunswick through a system of accounting.

"There does exist such a thing as provincial Credit. The Constitution of 1867 recognizes it when it says that the province can borrow on its own credit (not on the credit of another province). If the province can borrow and thus go into debt — on its own credit, then it most certainly can avoid debt by the simple process of making use directly of its own credit within the limits of its jurisdiction."

Obviously, there is going to be any amount of screaming and threatening from orthodox Finance and from the Orthodox "professional" economists who work for orthodox finance; as well as from the media of communications which are generally owned or controlled by Finance. Let such a plan even so much as be whispered in any legislative chamber and the ensuing fury from those who will fight to the death to retain financial dictatorship, will simply be appalling.

However, the solutions of orthodox finance lead only to the strengthening of Financial dictatorship and to the even greater impoverishment of the people.

New Brunswick's plight, if allowed to continue, will most certainly lead to its extinction as a political and cultural entity. And if New Brunswick disappears, which province will be next? Newfoundland which such a few short years was released from the guardianship of Great Britain? Or the other Maritime provinces which are scarcely better off than New Brunswick. Will they too come under the central authority of the federal government?

And how much longer will the remaining, stronger provinces be able to sustain the staggering national debt which is growing by the billions every decade? Will they too follow the path leading to a supreme central government holding an iron grip on the entire country without the cushion of lesser governments to shield the individual and the family from the brutal tyranny of the omnipotent State's bureaucracy?

The proposals of Social Credit are the only solution to this desperate plight of New Brunswick. And this plight of New Brunswick is one which ultimately all forms of lesser governments must face as long as orthodox Finance is allowed to go its way unhindered.

Rougemont Quebec Monthly Meetings

Every 4th Sunday of every month, a monthly meeting is held in Rougemont.

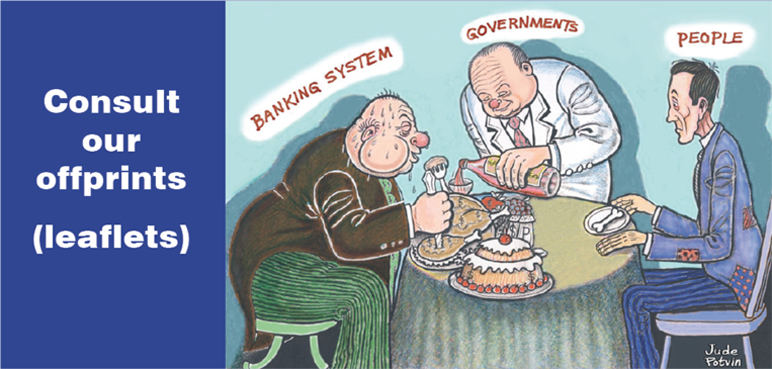

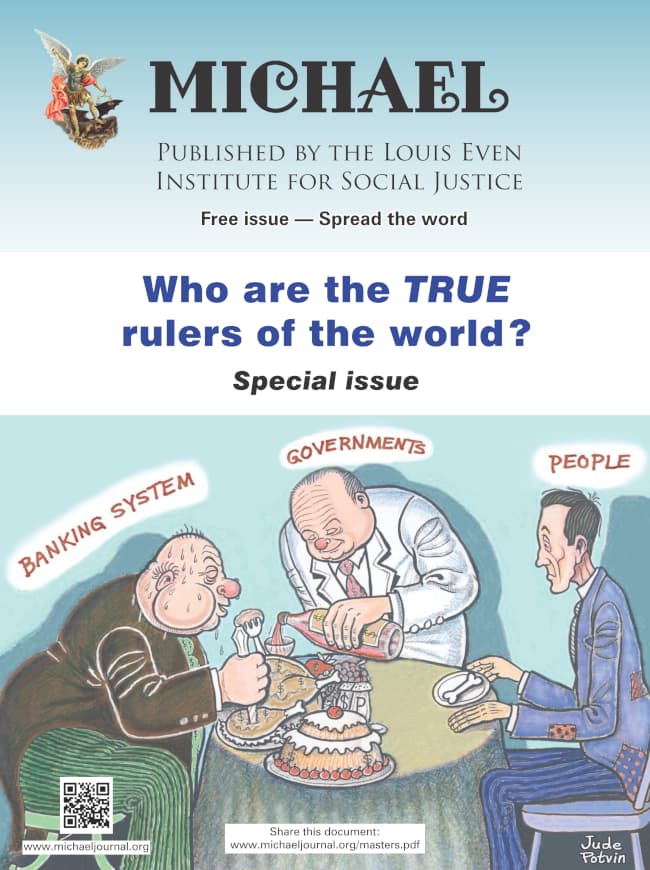

In this special issue of the journal, MICHAEL, the reader will discover who are the true rulers of the world. We discuss that the current monetary system is a mechanism to control populations. The reader will come to understand that "crises" are created and that when governments attempt to get out of the grip of financial tyranny wars are waged.

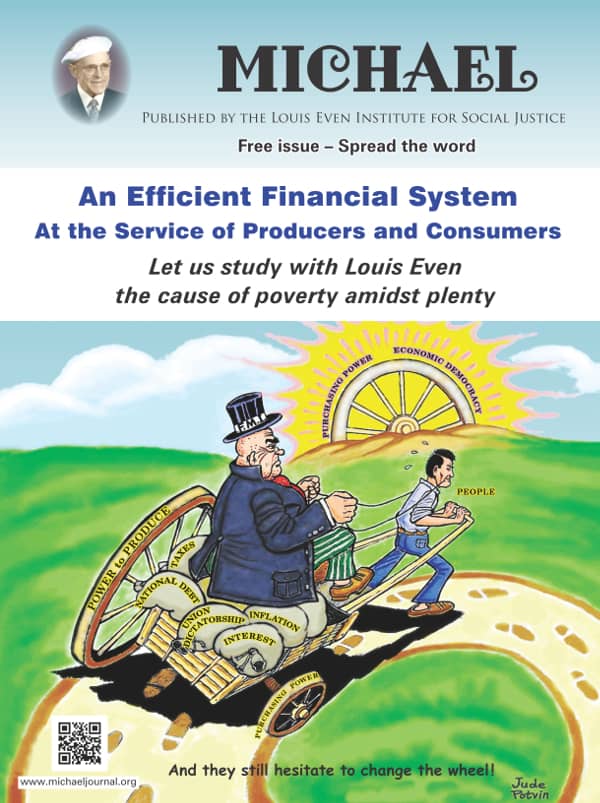

In this special issue of the journal, MICHAEL, the reader will discover who are the true rulers of the world. We discuss that the current monetary system is a mechanism to control populations. The reader will come to understand that "crises" are created and that when governments attempt to get out of the grip of financial tyranny wars are waged. An Efficient Financial System, written by Louis Even, is for the reader who has some understanding of the Douglas Social Credit monetary reform principles. Technical aspects and applications are discussed in short chapters dedicated to the three propositions, how equilibrium between prices and purchasing power can be achieved, the financing of private and public production, how a Social Dividend would be financed, and, finally, what would become of taxes under a Douglas Social Credit economy. Study this publication to better grasp the practical application of Douglas' work.

An Efficient Financial System, written by Louis Even, is for the reader who has some understanding of the Douglas Social Credit monetary reform principles. Technical aspects and applications are discussed in short chapters dedicated to the three propositions, how equilibrium between prices and purchasing power can be achieved, the financing of private and public production, how a Social Dividend would be financed, and, finally, what would become of taxes under a Douglas Social Credit economy. Study this publication to better grasp the practical application of Douglas' work.  Reflections of African bishops and priests after our weeks of study in Rougemont, Canada, on Economic Democracy, 2008-2018

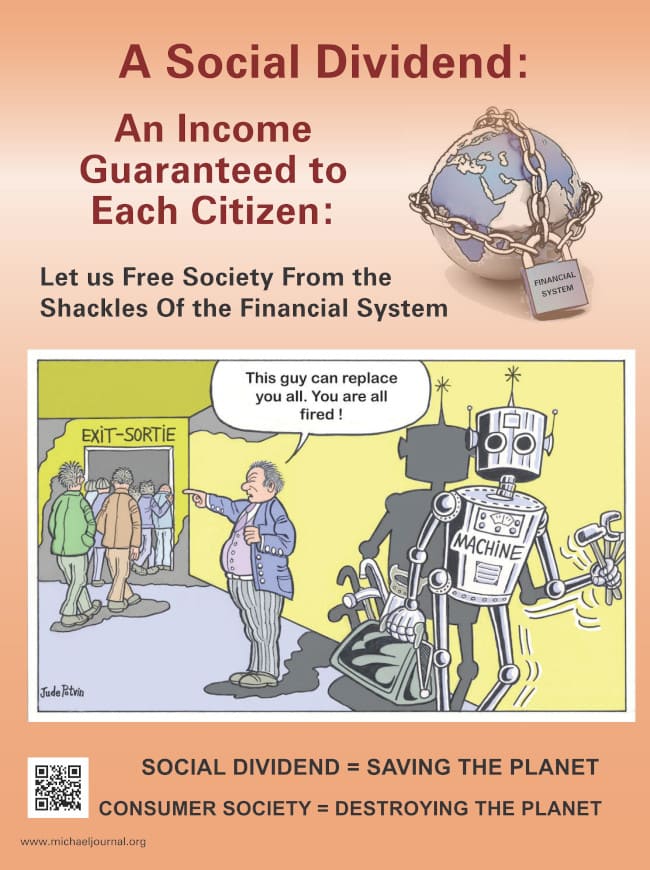

Reflections of African bishops and priests after our weeks of study in Rougemont, Canada, on Economic Democracy, 2008-2018 The Social Dividend is one of three principles that comprise the Social Credit monetary reform which is the topic of this booklet. The Social Dividend is an income granted to each citizen from cradle to grave, with- out condition, regardless of employment status.

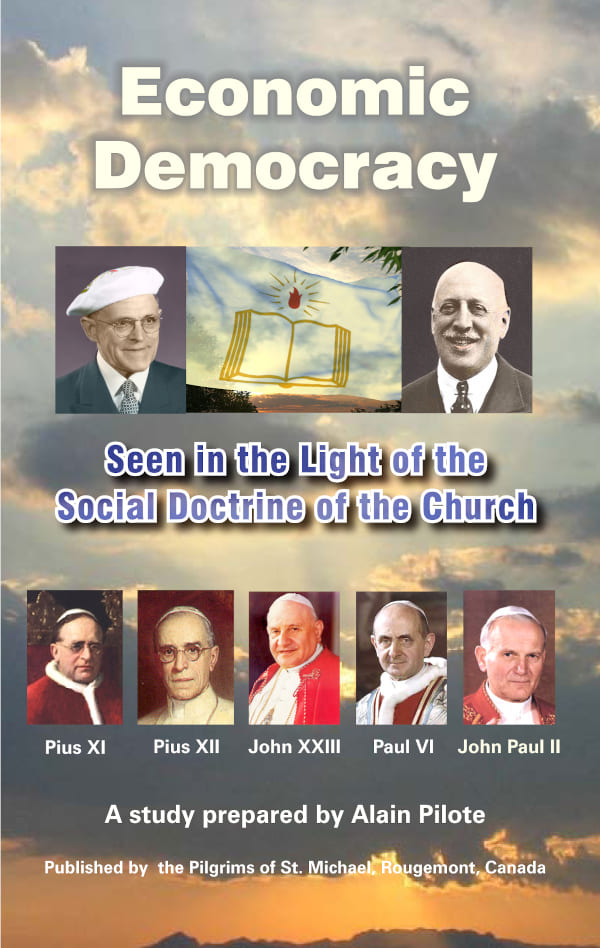

The Social Dividend is one of three principles that comprise the Social Credit monetary reform which is the topic of this booklet. The Social Dividend is an income granted to each citizen from cradle to grave, with- out condition, regardless of employment status. Economic Democracy is a book to explain Social Credit in lessons presented in logical order so it may be easier to the reader to grab the main principles of Social Credit rapidly and somehow easily.

Economic Democracy is a book to explain Social Credit in lessons presented in logical order so it may be easier to the reader to grab the main principles of Social Credit rapidly and somehow easily. In This Age of Plenty deals with Social Credit, but it does not exhaust the topic. Social Credit principles address social and political matters, as well as, or even more so, than economics and will put civilization on a new course.

In This Age of Plenty deals with Social Credit, but it does not exhaust the topic. Social Credit principles address social and political matters, as well as, or even more so, than economics and will put civilization on a new course. From Debt to Prosperity outlines briefly the economic analysis and constructive proposals known as Social Credit.

From Debt to Prosperity outlines briefly the economic analysis and constructive proposals known as Social Credit. Subscribe

Subscribe