The following is from a lecture given to The Pilgrims of St. Michael in Quebec, Canada in March 2005 by Mr. François de Siebenthal, an economist and Consul General of the Philippines. Mr. de Siebenthal, from Switzerland, demonstrated how easily a Local Bank can be established with the use of simple index cards. Mr. de Siebenthal has toured several countries to explain this system to interested audiences.

The use of index cards is a simple method of facilitating the exchange of goods and services without bending the knee to the digital age. Local debt-free banking is an idea whose time has come. Read this article to see that Economic Democracy is no longer just a theory. It is being implemented in regions around the world. Debt-free Local Banks are multiplying.

(As you read this essay please recognize that the term Social Credit was first used to describe a system of monetary reform developed by Clifford Hugh Douglas more than 100 years ago. The Chinese Communist Party has co-opted the term to describe something very different.)

I will now teach you how to open a Local Bank using Social Credit principles. It is very easy to do and anyone can do it.

In the past, Local Banks in Switzerland were established by farmers. The banker was also the farmer, the bank was in a farmhouse, customers were farmers and the owners of the bank were the same farmers. These little banks in Switzerland are the third largest banking system operating in the country and are the best managed because overhead is very low. Since the banks are very small and located in family farms, and because armored vehicles and security personnel are unnecessary, these banks are very efficient. These little banks can also be found in Austria and some other countries.

You know that money is created in the form of debt with added interest and you probably agree that interest kills. The International Labor Organization in Geneva states that every day 5,000 people die in the workplace. That is more deaths each day than the number who died in the Twin Towers. Each day! We know that because of the defects of capitalism and the demands of modern production there are many tragic and unnecessary workplace deaths. I am not including the suffering and death caused by stress, psychological problems, suicides, alcoholism, drugs, and the negative effects on children at home who have no supervision because both the father and the mother must work.

You can imagine that a system without added interest charges would save a great deal of money. Interest payments cost at least three hours every day for each one of us and increase the cost of housing by a factor of two or three.

I am here to teach everyone how to start a Local Bank. These banks have been launched in parts of Switzerland, Madagascar, Africa, the Philippines, Poland and Canada. They have been so successful that the World Bank and the International Monetary Fund are attacking them. In the Philippines there are attacks from the government and the print media. We can presume, due to these attacks, that Local Banks are of interest to many of us!

How to begin? What we did first was to listen to the people and so we asked what their real needs were. What ARE the real survival needs in Madagascar for example? In most of these countries some do not have sufficient resources to survive. We also must adapt to the culture and local conditions of the population.

Social Credit monetary reform would answer the real basic needs of these poor countries. After listening, we say that we have something that can help. It is not a magic wand that will give them paradise on earth, but it is a system that will guarantee each individual an access to the basic necessities of life and allow the poorest countries to make use of their resources for their own populations.

The main thing is to look for the Kingdom of Christ and His justice: "But seek first the Kingdom of God and His righteousness, and all these things will be given you besides" (Matthew 6:33). With local exchange systems we are really dealing with justice; the justice of God. Work for justice, and everything else will follow!

At this point, I would like to show the 5-franc coin that is currently in circulation in Switzerland. On one side there is the Swiss cross, which represents the Kingdom of Christ. On the other side, social justice is represented by the image of William Tell, the Swiss national hero and liberator of the poor and oppressed. On the coin's edge, are written the words in Latin: "Dominus providebit — God will provide". This harkens to the verse in Matthew already mentioned.

In all our meetings to organize debt-free Local Banks, we must remind people that God provides and that He is indeed very generous. In the Philippines, for example, three crops of corn can be grown in one season. One seed will produce three stalks which in turn yields 200 seeds. For one seed, God gives 200. Ten seeds yield 2,000; one hundred produce 20,000. Three crops per year (20,000 X 3) provides a 60,000% increase! Think about it: the banker will probably give you 6%. See God's generosity?

It is important to remember that the earth is generous and that there is enough room for everyone on the planet. There are fish in the sea and birds in the air. The tilled earth provides food generously. The earth is capable of feeding many times the world's population. We have a problem not of quantity but of distribution.

In Switzerland the system of small banks works. There is also another system in place: a parallel money which is called Wir, which is a German noun translated as We in English. This money has been in existence since 1933. It was created during the money crisis, and it is working very well. It is parallel money. Few know about this money. Switzerland, the poorest country in the world as far as natural resources are concerned, is one of the richest in the world because of its organization of small Local Banks and this type of parallel money.

The Catholic Church has always condemned the charging of interest on the loan of money, a practice called usury. As a matter of fact, the Social Doctrine of the Church, which provides the principles of justice applied in human affairs, is a little known teaching of the Church. The best kept secret perhaps is the encyclical letter, Vix Pervenit, issued in 1745 by Pope Benedict XIV. It was addressed to the Bishops of Italy on the subject of contracts. Usury, or money-lending at interest, is condemned in this document. In 1836, Pope Gregory XVI extended this encyclical to the entire Church. The text of this encyclical was destroyed in many countries of the world to hide this most well-kept secret of the Social Doctrine of the Church. It states:

The kind of sin called usury, which lies in the loan, consists in the fact that someone, using as an excuse the loan itself — which by nature requires one to give back only as much as one has received — demands to receive more than is due to him, and consequently maintains that, besides the capital, a profit is due to him, because of the loan itself. It is for this reason that any profit of this kind that exceeds the capital is illicit and usurious.

"And in order not to bring upon oneself this infamous note, it would be useless to say that this profit is not excessive but moderate; that it is not large, but small... For the object of the law of lending is necessarily the equality between what is lent and what is given back... Consequently, if someone receives more than he lent, he is bound in commutative justice to restitution..."

The principle is the same as in the tale of "The Money Myth Exploded": an account is created for each member of the community

The principle is the same as in the tale of "The Money Myth Exploded": an account is created for each member of the communityTo establish a debt-free Local Bank is very easy. Collect index cards or small booklets and a general ledger. In fact, we will do exactly what the five people in the tale of Salvation Island did when they realized they could create their own money.

The following system will allow any community or village to make financially possible what is physically possible in that community, that is to say, to create as much money as necessary to exchange goods and services. Just as in the tale, "The Money Myth Exploded", you can first use a blackboard to explain the system to people who wish to be part of a Local Bank and exchange system.

Next, distribute to each person an index card, which will be their bank account (see Figure 1, a blank card). You can use any type of card for bookkeeping that is small enough to put in one's pocket or purse. This will be the money and, at the same time, the way to create local money without interest. It is very important to emphasize - without interest!

It is a good idea to distribute pens in poor regions. Write on the card basic personal information, such as the name, address, card number (which becomes your bank account number), birth date and signature. The signature proves that you are the owner of this card; even if you lose it, nobody else can use it, for as you will see later, your signature is required on the cards — yours and that of the person with whom you are exchanging goods or services — every time you make a transaction.

The first thing to do after the cards are distributed is to assign numbers to each person so that everyone in the room has a number. The first row can have the numbers 1, 2, 3, and so on. Each person states the next number in sequence and everyone writes his number on his card. One person in charge of the ledger for the community writes all the names in the ledger with the corresponding account numbers. This will be your bank account number. It is like a football team — you give a number to everyone, and this number will match the name on your card.

Add a phone number and email address, if applicable. One's occupation can be cited and other jobs you could do or services you could offer can be added. This information can be used if one wants to create a catalogue of all the goods and services offered in the community. On the back of the card, we would have the address and phone number of the Local Bank.

Now, in the other columns, you have the date, the reason for the transaction, a column to show the money you spend (which is money withdrawn from your account), the account number and signature of the person with whom you have completed a transaction and a column for the money coming in to you. You can see that this is very simple.

Figure 2 — Tom Smith's card

Figure 2 — Tom Smith's cardNow to understand better how it works, we have an example you can look at (figure 2, Tom Smith's card). The first amount written down on your card will be the Social Credit Dividend, given periodically, such as once a month, to every member of the community. The Dividend represents the community's common heritage which rightfully belongs to everyone: progress, life in society and natural resources. This amount is to be determined by the community, and must cover the basic necessities of life. So, on the first line, you see a date, the reason (a Social Dividend "deposit"), nothing in the money-out column (you draw a line; it is money that you receive, not money that you spend), the number and signature of the person giving you that money (in this case, the signature of the Local Bank or its director, and for the sake of the example, the number "0" was allocated to the bank). In the last column, see that $100 was deposited. (The bank has given you a Dividend of $100.) This transaction has also been noted in the bank's central ledger.

Let's go to the next entry. Let us suppose that Tom Smith wants to buy 50 kilos of apples for a cost of $50, from Paul Jones. Note the date of the transaction, the reason (purchase of apples), the amount spent ($50), the account number and Paul Jones' signature. (Paul Jones was assigned account number 2.) Paul signs his name on Tom's card and Tom signs his name on Paul's card.

Figure 3 — Paul Jones'card

Figure 3 — Paul Jones'cardEvery transaction always involves two cards, and therefore two signatures. So, a purchase for you on your card will be a sale for the other person involved in the transaction on the other card. If you look at Paul Jones' card (figure 3), the reason for the transaction will be "sale of 50 kg of apples"), and the $50 will be noted in the money-in column, not the money-out. And Tom Smith's signature will appear at the end of the line.

Now, let us suppose Paul Jones has a chair that needs to be fixed and goes to see Tom Smith who is a carpenter. Tom Smith agrees to do the job for $10. So you will have on both cards the reason for the transaction (chair repair) and the amount ($10) written on each card — as money that comes in on one card and money that goes out on the other. And the examples could go on and on.

This system is best to present to the audience during the meeting for the launch of the Local Bank. The best thing for you now is to train yourself with such a card. When the cards are distributed, you put your name on the card — you do not need to put all the other details. And you make transactions with your neighbours. You buy and you sell. You will soon see that you are using the same money-creation system that the banks use. They do the same digitally in the privately owned banking system, but you will do your transactions without any interest charges in a bank which you own.

Train yourself for a while with your neighbours on how to create local money. The training period is very important. Take at least 15 minutes for this training period until everyone in the room understands. It is very important! In the Philippines, the young people went to the old people to teach them as some of them were not able to read or write, but they were able to understand this system because it only uses figures. Even if they do not know how to write letters, they know how to write numbers.

A contract is established every time you create money. You have, at the same time, proof of the contract, a commitment with the signature, and the number to confirm the signature.

You control the system. Money creation is under your control and the control of your local community. You know each other and you can create as much money as is necessary to meet your needs. So what is physically possible has now become financially possible. Your community will never lack money.

This system is the same that the banks use to create money, but you will control yours! You control it without interest! It is very cheap and efficient. You can create any amount of money according to the available production and services. You can exchange any number or type of goods and services. You own the money-creation system!

This is even more efficient than the actual system because, for example, there is a cost to print bank notes. Just one line of printing machines with special ink, special paper, etc. costs $100,000,000 US. This amount is saved with our system. It is even better than a bank note because you have your name on it. If you lose your card, someone will phone you telling you he "found your money". The person who finds your money can do nothing with it because your signature is necessary. It really is your money.

You cannot dispossess someone who has lost his money. If the money (the index card) is destroyed by fire or other means, you can reconstruct a card using information from other cards. All cards are consolidated in the local bank ledger. This means that if your bank card is destroyed, or lost, you can reconstruct it with the accounts of others because other account holders have a record of every transaction they did with you. You can rebuild your accounting books and reclaim your assets. This is an even better method than the actual system with bank notes. And you have, naturally, no interest. This means every transaction will be cheaper because, today, interest charges kill people.

In my presentation I say to the audience: "Do you want to own a bank? Yes? Who does not want to be the owner of a local bank? I assume that everyone wants to be the owner of a bank. You can be the owner of a bank, like we did in the Philippines, Madagascar, Switzerland, and Poland." But to be the owner of a bank, it is necessary to have a management team and people who are willing and ready to act as auditors. So now I ask "Who will volunteer to act as managers and auditors of the bank? I need at least three managers (a director, secretary and a treasurer) and two auditors (who periodically verify the bank's books). Now, those who are willing to function as managers and auditors of this Local Bank owned by the local community, please come to the front of the room."

It was very interesting to see how many people were willing to act and to take the responsibility of running the bank. In Poland, we had so many people who came on the stage, it was incredible. In the Philippines, many people volunteered to fill these positions also. So be sure to have seats in front so the new managers and auditors will be able to sit down. It is the community that finally chooses the people who will be on the board of the bank, people they can trust and who have enough skills to do the job.

In Madagascar, we established a bank in one of the poorest villages in the country, and now we are receiving great reports from the bank's management team. They understood, and took the responsibility of their new bank very seriously.

Being the manager of a Local Bank is straightforward. Your only task is to be in charge of the bank ledger. There is no need for a safe, bulletproof windows, armored trucks nor armed bodyguards to carry the money, etc. The only thing you have to keep in your house is the bank ledger.

At this stage you have the management team, the auditors and the bank's customers. It is now important to put in writing fair prices for basic goods and services in the area. This is to be decided by the general assembly/customers. It is also very important to put in writing how the profits will be divided within the community because this bank will create money as any other bank and can create money for production. Thus the people, when they have a lot of pluses (money-in) on their cards, can invest those pluses in various projects, and those projects will yield more abundant production. So it must be put in writing how the profits of this abundance will be distributed. This way, the people will be more eager to share.

In the Philippines a rice producer who very well understood the system, signed a contract to share 70% of the profits from his rice production with customers/general assembly, keeping only 30% for himself. It was really astonishing for me to see this generosity. A priest explained to me that when there is no interest charged, no usury in other words, the producers are very happy because, in those countries, usury can climb up to 1,000% per year; that means 20% a week is stolen by usurious practices. Because we now have a small banking system without usury, everyone is happy and everyone can share more. Now all this money will not go to the usurer who was doing nothing except stealing 1,000% per year.

This system reminds us of the parable of the dishonest steward. In the Gospel of Luke (Chapter 16) the steward says to his master's debtors: "Here is your promissory note. Sit down and quickly write half the sum that you owe to my master." The only difference is that with our debt-free Local Bank, everything is done honestly. It is working! In fact, in the Philippines it is working so well that we now have more than 15 Local Banks [as of March 2005]. And some in the media and the government (from population control agencies) are attacking this system. That gives us free advertising and much publicity. Those attacks have a silver lining in spreading the system because now everyone is talking about Local Banks.

It is the love of money that is the root of all evil, and with this system, there is less the notion of money being a thing folded in your wallet. This way, you love your money less because it is genuinely only a means to facilitate exchanges. You can exchange any goods and any services. It is not so easy to love an index card or booklet which is really just your handwriting and the signatures of others. It is not as easy to love this piece of paper as it is to love gold or coins or banknotes. This system offers a way to side step the root of all evil, the love of money.

This card system also provides a measuring stick for the creation of money. Just as a ruler measures meters or feet, you have a ruler now to create the money necessary for local community life in the form of a Dividend. With this system, you can allocate money for the basic needs of the poorest. The Dividend must be accepted by the general assembly. Normally we recommend giving a Dividend at least equal to the amount necessary to cover basic needs for the lives of the poorest, the sick and the old people present.

It is working. For example, in the Philippines they have chosen a Dividend of $100 US. The local economy has boomed now because there is enough money in the system.

We are looking for people to go all over the world to spread this good news. This good news makes the poor richer. This also makes local development possible. This too allows the poor to have as much money as they need for the physical needs of the local community. It is really a tool for liberation.

Naturally, in this process you need to pray, so we always ask the people to pray together before each meeting. Because of the prayers of the Rosary and all the prayers of all the Social Crediters since the foundation of the movement, it is really reaping much fruit.

We must work with speed. For example in the Philippines, the development has been rapid. Even though one Local Bank is a good thing, it is not enough. We need to spread on a regional level around a city. This way you can exchange all the goods, the food and services necessary to meet basic needs. It is now happening in the Philippines. We are really astonished that they have understood so well with just one month's teaching. They have already opened more banks than we did when we were there. Now we really need people to travel all over the world to spread this idea to others.

Mr. François de Siebenthal, from Lausanne, Switzerland, is in charge of the Institute of Monetary Studies. He is an economist, Consul General of the Philippines, Secretary General of the Consular Corps, and great friend of the journal, Michael. Moreover, Mr. de Siebenthal holds two other distinguishing titles: he is a Catholic and the father of eight children.

Rougemont Quebec Monthly Meetings

Every 4th Sunday of every month, a monthly meeting is held in Rougemont.

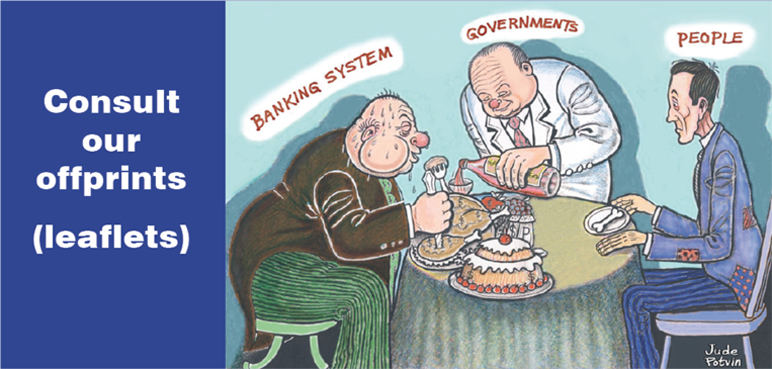

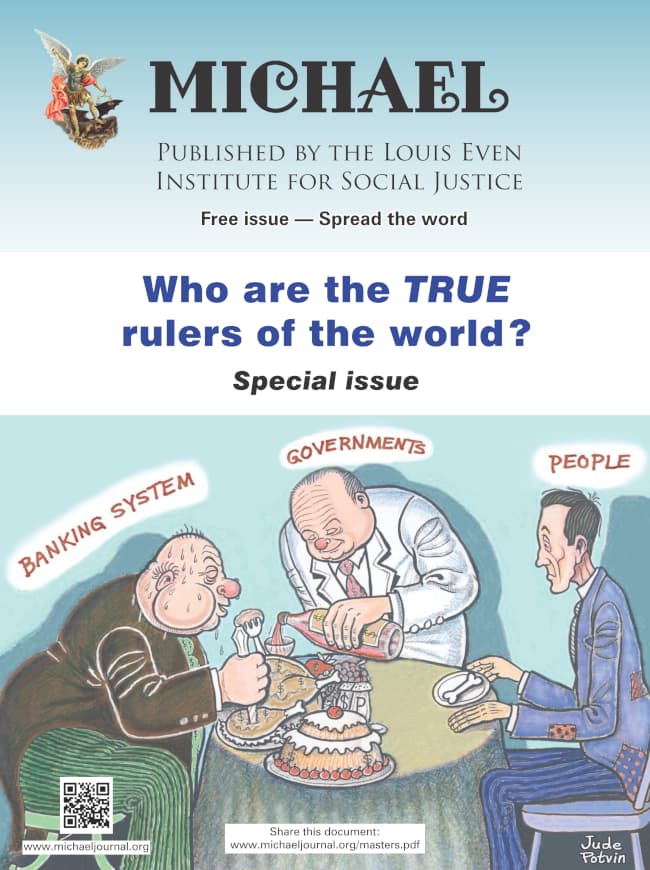

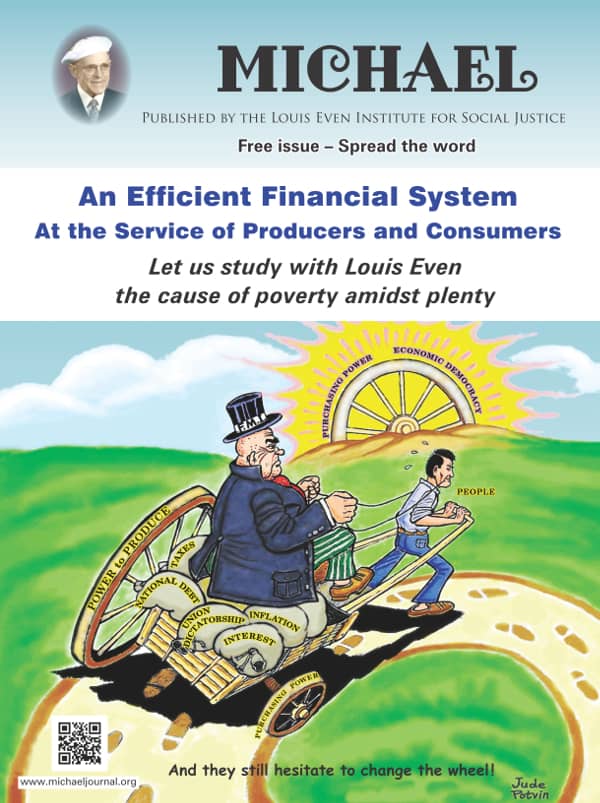

In this special issue of the journal, MICHAEL, the reader will discover who are the true rulers of the world. We discuss that the current monetary system is a mechanism to control populations. The reader will come to understand that "crises" are created and that when governments attempt to get out of the grip of financial tyranny wars are waged.

In this special issue of the journal, MICHAEL, the reader will discover who are the true rulers of the world. We discuss that the current monetary system is a mechanism to control populations. The reader will come to understand that "crises" are created and that when governments attempt to get out of the grip of financial tyranny wars are waged. An Efficient Financial System, written by Louis Even, is for the reader who has some understanding of the Douglas Social Credit monetary reform principles. Technical aspects and applications are discussed in short chapters dedicated to the three propositions, how equilibrium between prices and purchasing power can be achieved, the financing of private and public production, how a Social Dividend would be financed, and, finally, what would become of taxes under a Douglas Social Credit economy. Study this publication to better grasp the practical application of Douglas' work.

An Efficient Financial System, written by Louis Even, is for the reader who has some understanding of the Douglas Social Credit monetary reform principles. Technical aspects and applications are discussed in short chapters dedicated to the three propositions, how equilibrium between prices and purchasing power can be achieved, the financing of private and public production, how a Social Dividend would be financed, and, finally, what would become of taxes under a Douglas Social Credit economy. Study this publication to better grasp the practical application of Douglas' work.  Reflections of African bishops and priests after our weeks of study in Rougemont, Canada, on Economic Democracy, 2008-2018

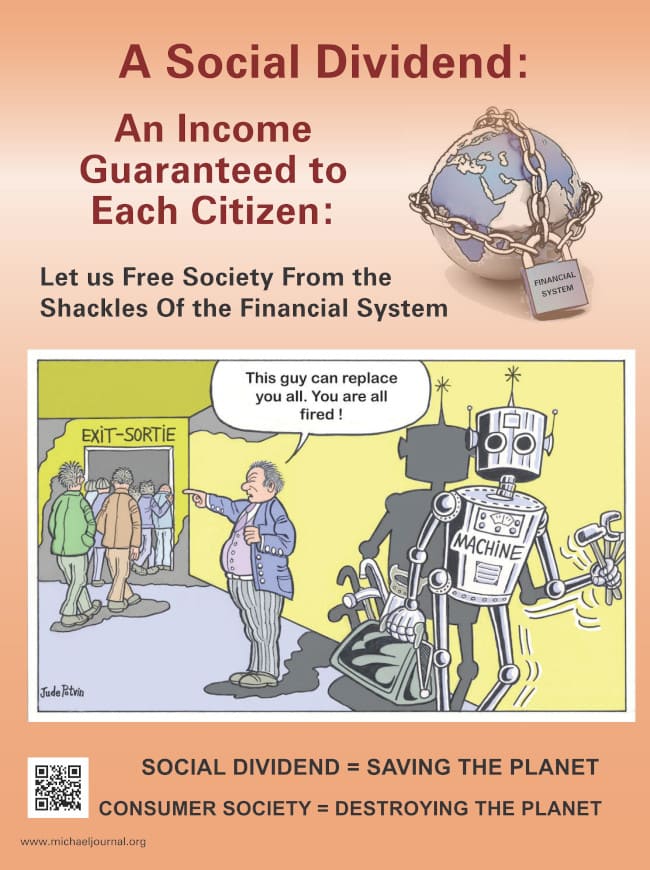

Reflections of African bishops and priests after our weeks of study in Rougemont, Canada, on Economic Democracy, 2008-2018 The Social Dividend is one of three principles that comprise the Social Credit monetary reform which is the topic of this booklet. The Social Dividend is an income granted to each citizen from cradle to grave, with- out condition, regardless of employment status.

The Social Dividend is one of three principles that comprise the Social Credit monetary reform which is the topic of this booklet. The Social Dividend is an income granted to each citizen from cradle to grave, with- out condition, regardless of employment status. Economic Democracy is a book to explain Social Credit in lessons presented in logical order so it may be easier to the reader to grab the main principles of Social Credit rapidly and somehow easily.

Economic Democracy is a book to explain Social Credit in lessons presented in logical order so it may be easier to the reader to grab the main principles of Social Credit rapidly and somehow easily. In This Age of Plenty deals with Social Credit, but it does not exhaust the topic. Social Credit principles address social and political matters, as well as, or even more so, than economics and will put civilization on a new course.

In This Age of Plenty deals with Social Credit, but it does not exhaust the topic. Social Credit principles address social and political matters, as well as, or even more so, than economics and will put civilization on a new course. From Debt to Prosperity outlines briefly the economic analysis and constructive proposals known as Social Credit.

From Debt to Prosperity outlines briefly the economic analysis and constructive proposals known as Social Credit. Subscribe

Subscribe

Comments (1)

Abri Dealdi

Reply