We know then that goods are conveyed from Producer to Consumer by means of money. Money is thus the connecting link between production and consumption. It acts as a bridge between the desire for goods on the part of the consumer and their supply on the part of the producer. We might say that money is the equalizing medium between desire and goods, enabling the one to be satisfied in terms of the other. It functions as a force which, like electricity running a motor, is invisible, and we see only its effects transforming desire, which is mental, into physical goods which represent the satisfaction of that desire.

From this it should be plain that money is something numerical, not a material substance. Money is not wealth, but a symbol of wealth and a means of measuring its value. Money gives us a method for applying number values to goods.

If we stick to our personal experience, we cannot fail to realize that money is only a ticket, a ticket authorizing us to go shopping in the Nation’s store of Wealth. Money entitles us to claim the wealth of goods in the store. A money-ticket is exactly like a railroad ticket except that a railroad ticket is only good for transportation while a money-ticket is good for anything in the store up to its stated value in prices.

“We thus arrive at a true conception of the nature of money; money is simply a social mechanism designed to facilitate orderly production and distribution. The money system is to all intents and purposes merely a system of tickets entitling the holders to goods and services. Above all, money as such is not a commodity; it has no intrinsic value apart from the function it performs, and to regard money as a commodity is proof of a radical misunderstanding of that function.”1

Money is NOT a commodity with substance, size and weight, like wheat or steel. Thinking about money as a commodity, such as gold, instead of as a measure of value, has caused much of our confusion today. For even “financial experts” agree that commodities fluctuate in value according to supply and demand, and thus no one commodity by itself is suitable as a single absolute measurement of value for all others.

Prof. Frederick Soddy says, “Gold is in all respects about the worst commodity to choose as a money standard.”2

Money is so important in our lives that we may well think of it as the keystone which holds together the whole of our economic structure. The reason why money is so important that people quarrel about it, is that these money-tickets are indispensable to our shopping. Money-tickets are just as necessary to our shopping as shopping is to our lives. In civilized society our lives depend on money and the money system. For without money that works, that is “sound,” we cannot touch any of the wealth that fills the shopwindows of America.

But to deserve the name “sound,” money must possess two important qualifications. For one thing it must have acceptability, which means simply that everyone who uses it has confidence that it can be exchanged for wanted goods or services. And secondly since it is the medium of exchange, we should expect to find money accurately expressing the current demand for available goods.

Any sort of a sound money system, in short, must reflect the true facts of production. It must provide enough of the means of exchange to keep goods moving from producers to the shoppers who consume the goods.

As we have already seen, there are mainly two kinds of money in use today. The first of these is currency, or tangible government money which circulates as coins; pennies, nickels, dimes, quarters, and dollar bills. The second is credit-money, or bank deposits circulating in the form of cheques.

Currency is only the pin-money of business. Credit-money (or cheques) is used in practically all large transactions, where coins or bills are not convenient. In fact, more than 90% of our business is done with cheques, or credit-money.

We know that currency is issued by the government as coins or printed bills, but many people do not know just where or how credit-money comes into existence. We use cheques because they are safe and handy, they can be written for paying an exact amount to specific individuals, and so long as they are acceptable we think no more about it.

Suppose we look into the source of this credit-money with which we do at least 90% of our buying and selling. Where is it born? We know that a cheque is an order against a bank balance. The bank balance consists of deposits credited to an account. These deposits themselves may be in the form of cheques drawn upon other accounts. No currency actually changes hands in paying for goods or services with this kind of money. Complicated transactions involving immense sums of money are handled purely by means of the bookkeeping carried on by the banks, entering credits and debits on their books. In their bookkeeping the banks credit and charge the accounts of their customers.

It is clear from this that whatever money was once intended to accomplish, by means of currency, it is a different story now that we write cheques. The cheque system today is simply a series of bookkeeping entries, and our monetary system functions mainly as the circulation of these cheques. We do almost all our business by means of bits of paper, which are evidences of Financial Credit. And this credit is itself created or destroyed in the bookkeeping process of the banks. “The cheque system is in itself a great advance upon the use of tokens in many ways. But its invention has resulted in the banks, not indeed coining money as that is quite unnecessary, but creating money without even the issue of printed notes...”3

“The method by which the banker makes money is ingenious and consists largely of bookkeeping.”4 This kind of money is born in a bank and dies in a bank. And the bank is responsible both for its birth and its death. “The banker creates the means of payment out of nothing.”5

The fact that banks create and destroy money by the bookkeeping process of issuing or cancelling credits is illustrated by any ordinary bank loan. Suppose we go to the bank to borrow $1,000. The banker passes judgment on our credit rating, accepts our note, and grants the loan, crediting our account exactly as though we had deposited this sum in cash. We are now “in debt” to our friend the banker. We owe him the $1,000 we have borrowed, plus the interest he charges for its use. We can then write cheques against our new account, and these cheques are acceptable as money.

Now the banks are permitted to lend up to ten times their actual cash reserve, and in so doing the banker “creates” in the case of our loan, $1,000 (less interest) in new money.

But when the time comes to repay this sum the credit he has extended to us is destroyed. We can no longer write cheques against it. Indeed, we must pay the banker promptly or forfeit whatever security has been placed with him as collateral. If we cannot pay, our security then passes into his hands. In other words, every bank loan creates a deposit and every repayment of a bank loan destroys a deposit. Loans are made and deposits created by crediting the borrower’s account in the banker’s book. And the money thus created is destroyed in the same way, by debiting the borrower’s account. What has it cost the bank to lend us $1,000? Nothing but the expense incurred in its bookkeeping.

As a result of the bookkeeping process of the banks, new money is constantly being created and destroyed. And this money, said by the Encyclopedia Britannica to be created “out of nothing,” is really being manufactured out of little more than pen, paper, confidence, and a bottle of ink.

This bookkeeping process, the banking method governing the birth and death of money, is clearly described by Reginald McKenna, Chairman of the Midland Bank of London and former Chancellor of the Exchequer: “The amount of money in existence varies only with the action of the banks. Every bank loan creates a deposit...” and further, “there is only one method by which we can add to or diminish the aggregate amount of our money... The amount of money in existence varies only with the action of the banks in increasing or diminishing deposits. We know how this is effected. Every bank loan and every bank purchase of securities creates a deposit, and every repayment of a bank loan and every bank sale destroys one.”6

When we think of our own hard-earned personal bank accounts we perhaps imagine that our deposits are used by the banks to create new credit-money. But the banks do not, as many people believe, lend such deposits. By virtue of their privilege of lending up to ten times their cash reserves, banks create Financial Credit which in their bookkeeping becomes a DEBT against the borrower.”7

“It is not unnatural to think of the deposits of a bank as being created by the public through the deposit of cash representing either savings or amounts which are not for the time being required to meet expenditure, but the bulk of the deposits arises out of the action of the banks themselves, for by granting loans, allowing money to be drawn on an overdraft or purchasing securities a bank creates a credit in its books which is the equivalent of a deposit.8

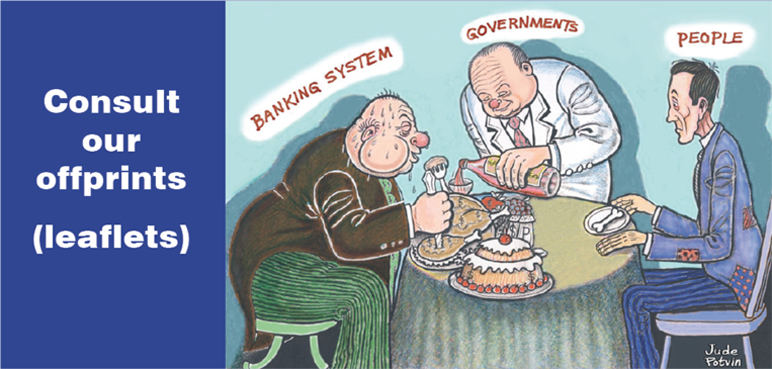

“Although, then, we are stressing the function of the banking system as a manufacturer of money, it is far from our object to impress the reader with any suspicion that such manufacture is criminal. —Our object is to impress the reader with the importance of the fact that it is a private body, not responsible to the nation, which actually manufactures and controls the manufacture of money, and by so doing controls the nation’s means of life.”9

Money circulates. This is a fact familiar to every one. In the economic system money may well be compared to the blood of the human body. Money in business is equally as vital as the blood in our bodies. It circulates, carrying life and vitality in its flow. Money is the medium of exchange. Business cannot survive without exchange. Exchange implies activity, and this activity is the flow of money, its circulation. The flow cannot cease, for money satisfies desire only when it is exchanged for goods and services. It has no inherent value in itself. Money itself cannot be worn or eaten but it can buy clothing to wear and food to eat. When money ceases to flow, its power to satisfy desire dies, exactly as we die when our blood stops circulating. Only so long as money circulates is business alive and healthy.

We know the time blood takes to circulate through the human body. We measure its circulation by our pulse rate. And in just the same way it takes time for money to circulate through business. Time and flow taken together give us a rate of flow, and this rate of flow is the way we measure the speed of the circulation of money.

But the likeness between money and blood is still closer. For both of them circulate; that is, the course of their flow is circular. Money tends to flow in a circle through business. Its circulation begins in a bank, since it is in the bank that most of our money is born. The banker, for example, makes a loan to a producer. The producer pays his workmen, executives and shareholders, who presently appear as shoppers, consumers of goods in the retail market. The retailer then pays the wholesaler, who in turn pays the producer, who at length repays his loan to the bank. Whereupon that amount of credit is destroyed until the bank makes a new loan, when it creates more new credit.10 Then the circle is repeated. And business is dependent for its existence on this life-blood circulating in its economic body.

Now our study of money grows exciting, for here we come face to face with Debt. We know debt well, for it is always at our door. And it poses as our friend credit, a wolf in sheep’s clothing. More than that, Debt plagues us always, since every bank loan, in creating a deposit, at once puts the borrower into the clutches of debt. Banks, it is true, create “credit,” which they are said to extend to borrowers. But the bank’s “credit” becomes the borrower’s debt. Strictly speaking, therefore, most of our business is done on debt, because the money thus created is issued as loans which must be repaid with interest.

The old Biblical tale of Noah and the Flood has its modern parallel. We are told that in Noah’s day the world was submerged under great waters. But our modern flood is even greater than Noah’s and just as real. For in our day we are steadily sinking under a deluge of debt. “We are not thinking of War Debts, or of International Debts, or of any relatives of these which may be in the limelight at any given moment, but of the system itself by which all money is debt. It is a debt to the banking system.”11

Struggle against this as we may, so long as money comes into being as a debt to the banking system we are its slaves. As Colbourne says, “Even our vocabulary is perverted. When a bank is said to extend you credit it is doing nothing of the kind; it is extending you debt.”12

It may be a disturbing thought to realize that the bulk of our money is debt-money, created by the banking system on the basis of the country’s resources and its ability to deliver wanted goods. But however disturbing it may be, it is nevertheless true. Our money is a circulating evidence of debt to the banking system. This is the solid fact which we must grasp: The bulk of our money is Debt-Money.

Is it any wonder that we sink in a flood of debt when every article of wealth we buy must be paid for with money which itself is debt? Debt surrounds us from birth to the grave. We cannot be rid of its grip because of the ingenious financial device called INTEREST.

The deluge of our present debt can never be drained away because interest requires that the debtor repay more than has been loaned him. The process by which Debt-Money is created is cumulative — it grows. The debt cannot be liquidated because it grows faster than business can repay it. It can never be repaid, now or at any other time.

Thomas A. Edison is authority for the statement, “In all our great bond issues the interest is always greater than the principal.” The total of principal and interest, which is more than the original loan, can be met only by the creation of fresh debt. Thus debt breeds more debt, and the more we struggle the deeper we sink.

But our situation, bad as it appears now, is growing worse. For example, when we try to use this borrowed money to draw wealth from the shopwindows of the nation it becomes impossible, at the same time, to use the money to draw wealth from the shopwindow and to repay the debt. If we borrow $5.00 to buy a pair of shoes, we have to choose between buying the pair of shoes and repaying the debt. If we choose to buy the shoes, we still owe the debt of $5.00. We can either have the shoes or pay the debt but we can’t do both at once.

But this is not the whole story. Business depends upon the debt-money of the banking system. Every dollar loaned to business must be recovered in prices. “Now, money is never borrowed except to be spent; but, as it must subsequently be repaid, the borrowers have to spend it in producing, or inducing the production of, something that can be sold; which means that the harder the community works and the more it produces, the deeper it goes into debt to the banks.”13 So debt mounts at the expense of our ability to buy goods.

“It must, I think, be quite obvious to anybody that, if the world as a whole is consistently getting further and further into debt, it is not, as the ordinary business man would say, paying its way. — The public is paying all that it can, and buying what it can. The failure to pay more is therefore forcing the destruction of some of it and at the same time it is piling up debt ...”14

How fast does debt grow? “In the 17th century, that is to say, in the century in which the Bank of England was founded, the world debt — and we have plenty of accurate figures with regard to these matters — increased 47 per cent. The Bank of England was founded only at the end of the 17th century.”

“By the end of the 18th century the world debt had increased by 466 per cent, and by the end of the 19th century the world debt, public and private, had increased by 12,000 per cent; and, according to some very exact calculations which have been carried out by a quite irreproachable professor of industrial engineering of Columbia University, Professor Rautenstrauch, taking the year 1800 as the origin and taking one hundred years as the unit, the world debt is now increasing as the fourth power of time; that is to say, increasing as time goes on, not as the square of time and not as the cube of time, but as the fourth power of time; and that is in spite of the numerous repudiations of debt, the writing down of debts which takes place with every bankruptcy, and other methods to write off debts and start again.”15

But we must not miss the one vital point which gives the key to this dilemma. The Debt-Money created and destroyed by banks is called “Financial Credit,” and in this term it is the word “financial” that deserves our attention. The deluge of debt is purely financial debt since it is based upon what the banks call the “credit” they create.

Now we have already seen that there are two kinds of credit: Financial Credit and REAL CREDIT, and herein lies our key. It was to make this point clear that we defined both Financial Credit and Real Credit before we began to examine the money system.

Later on we shall have occasion again to return to our definition of Real Credit.

At this point we may well pause for a moment to sum up what we have found in the money system, and see what conclusions are possible. We can list our findings as follows:

The first conclusion that stands out from all of this is that a money system built on debt and interest can function in the long run only to create more debt. And this is precisely what has happened. The facts of experience confirm our findings.

It is worth pointing out that this curious device of interest is peculiar to finance alone. It has no parallel in nature. It is one of man’s inventions, and certainly not his happiest.

The second conclusion, which is perhaps not quite so easy to see, is that under this system a shortage of money is inevitable, making it increasingly difficult to buy goods. There are two fundamental reasons for this and we shall begin with the simpler of the two.

1) C. M. Hattersley, This Age of Plenty, p. 37.

2) Prof. Frederick Soddy, Money versus Man, p. 53.

3) Prof. Frederick Soddy, Money versus Man, pp. 31-32.

4) C. H. Douglas, Oslo, Norway, Feb. 1935.

5) R. G. Hawtrev, Currency and Credit.

6) Speech at General Meeting, Midland Bank, Ltd., Jan. 25, 1924.

7) One of the greatest authorities on banking, H. D. McLeod, tells us in his book, The Theory and Practice of Banking, that — “The essential and distinctive feature of a ‘bank’ and a `banker’ is to create and issue credit payable on demand, and this credit is intended to be put into circulation and serve all the purposes of money. A bank, therefore, is not an office for borrowing and lending money; but it is a manufactory of credit.” “In the language of banking a deposit and an issue are the same thing.” “It is commonly supposed that a banker’s profit consists in the difference between the interest he pays for the money he borrows, and the interest he charges for the money he lends. The fact is, that a banker’s profits consist exclusively in the profits he can make by creating and issuing credit in excess of the specie he holds in reserve. A bank which issues credit only in exchange for money, never made, and can by no possibility make, profits. It only begins to make profits when it creates and issues credit in exchange for debts payable at a future time.”

8) Report of the MacMillan Committee on Finance and Industry, presented to Parliament, June 1931, Paragraph 74.

9) Maurice Colbourne, Economic Nationalism, p. 138.

10) “Credit originates in production and is extinguished in consumption.” R. G. Hawtrey, Currency and Credit

11) Maurice Colbourne, Economic Nationalism, p. 146.

12) Economic Nationalism, p. 147.

13) H. M. M., An Outline of Social Credit, p. 25

14) C. H. Douglas, Oslo, Norway, February 1935.

15) C. H. Douglas, Oslo, Norway, February 1935.

16) (1) Practically all purchasing power comes into existence in the form of a bank credit. (2) Bank credits are created by the banks out of nothing.” H. M. M., An Outline of Social Credit, p. 20.

Rougemont Quebec Monthly Meetings

Every 4th Sunday of every month, a monthly meeting is held in Rougemont.

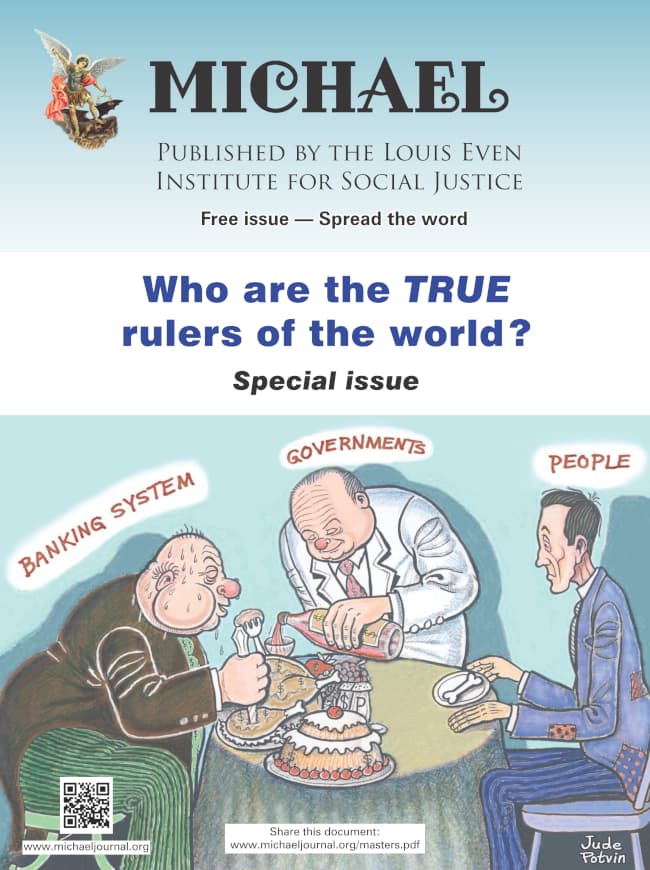

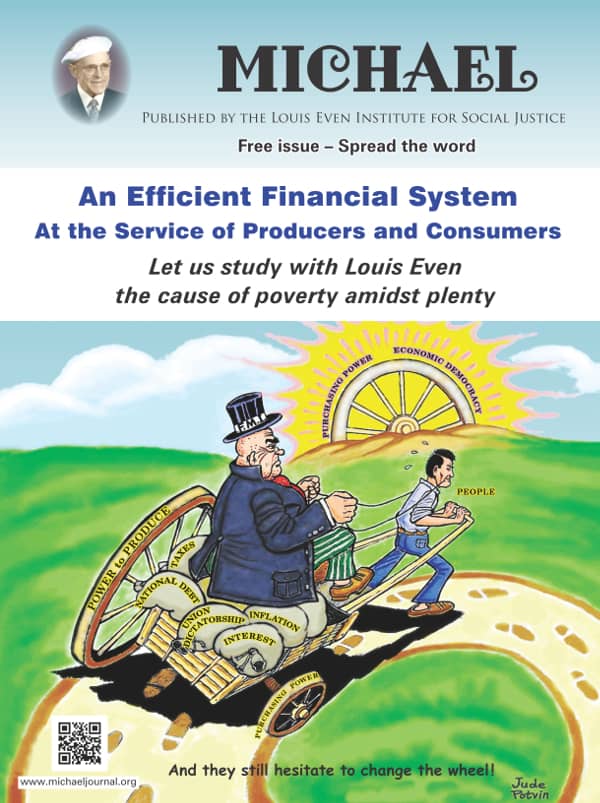

In this special issue of the journal, MICHAEL, the reader will discover who are the true rulers of the world. We discuss that the current monetary system is a mechanism to control populations. The reader will come to understand that "crises" are created and that when governments attempt to get out of the grip of financial tyranny wars are waged.

In this special issue of the journal, MICHAEL, the reader will discover who are the true rulers of the world. We discuss that the current monetary system is a mechanism to control populations. The reader will come to understand that "crises" are created and that when governments attempt to get out of the grip of financial tyranny wars are waged. An Efficient Financial System, written by Louis Even, is for the reader who has some understanding of the Douglas Social Credit monetary reform principles. Technical aspects and applications are discussed in short chapters dedicated to the three propositions, how equilibrium between prices and purchasing power can be achieved, the financing of private and public production, how a Social Dividend would be financed, and, finally, what would become of taxes under a Douglas Social Credit economy. Study this publication to better grasp the practical application of Douglas' work.

An Efficient Financial System, written by Louis Even, is for the reader who has some understanding of the Douglas Social Credit monetary reform principles. Technical aspects and applications are discussed in short chapters dedicated to the three propositions, how equilibrium between prices and purchasing power can be achieved, the financing of private and public production, how a Social Dividend would be financed, and, finally, what would become of taxes under a Douglas Social Credit economy. Study this publication to better grasp the practical application of Douglas' work.  Reflections of African bishops and priests after our weeks of study in Rougemont, Canada, on Economic Democracy, 2008-2018

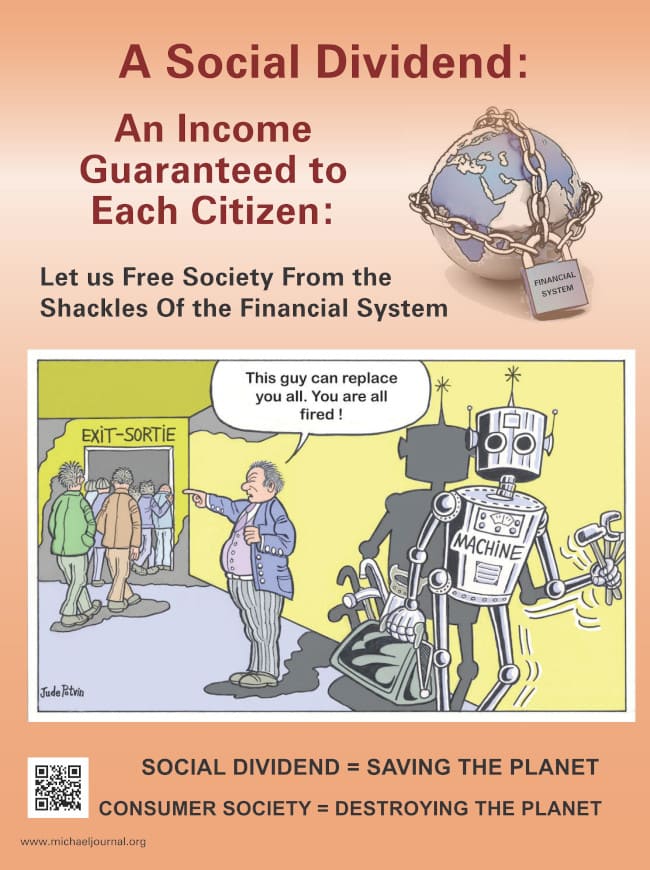

Reflections of African bishops and priests after our weeks of study in Rougemont, Canada, on Economic Democracy, 2008-2018 The Social Dividend is one of three principles that comprise the Social Credit monetary reform which is the topic of this booklet. The Social Dividend is an income granted to each citizen from cradle to grave, with- out condition, regardless of employment status.

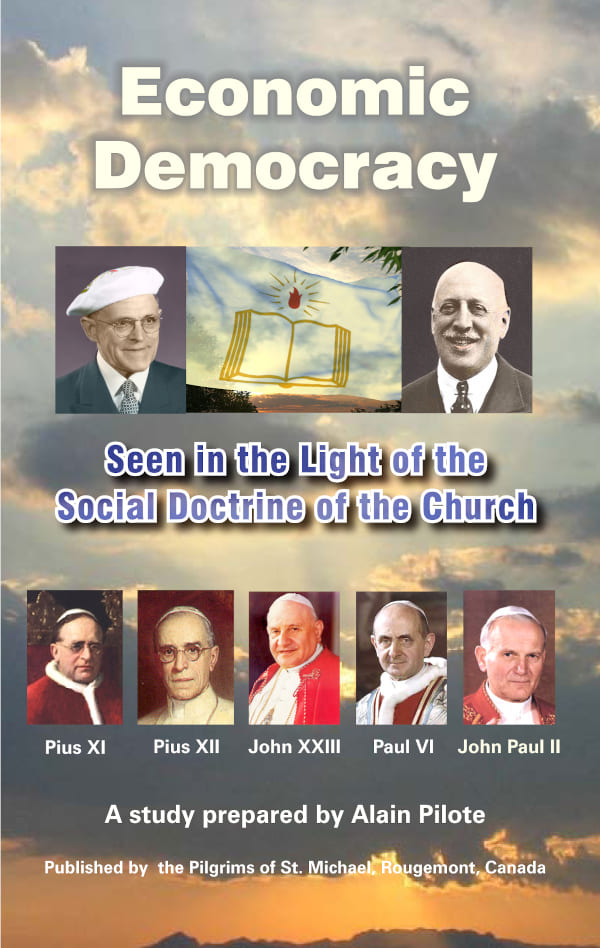

The Social Dividend is one of three principles that comprise the Social Credit monetary reform which is the topic of this booklet. The Social Dividend is an income granted to each citizen from cradle to grave, with- out condition, regardless of employment status. Economic Democracy is a book to explain Social Credit in lessons presented in logical order so it may be easier to the reader to grab the main principles of Social Credit rapidly and somehow easily.

Economic Democracy is a book to explain Social Credit in lessons presented in logical order so it may be easier to the reader to grab the main principles of Social Credit rapidly and somehow easily. In This Age of Plenty deals with Social Credit, but it does not exhaust the topic. Social Credit principles address social and political matters, as well as, or even more so, than economics and will put civilization on a new course.

In This Age of Plenty deals with Social Credit, but it does not exhaust the topic. Social Credit principles address social and political matters, as well as, or even more so, than economics and will put civilization on a new course. From Debt to Prosperity outlines briefly the economic analysis and constructive proposals known as Social Credit.

From Debt to Prosperity outlines briefly the economic analysis and constructive proposals known as Social Credit. Subscribe

Subscribe