The huge public debt of the U.S.A., which is over 7,000 billion dollars (in 2004), makes every American aware of the urgency to correct the situation. But if politicians do not attack the root cause of the problem, on what causes the debt to increase, all their reforms will be useless, and the situation will even get worse.

The regular readers of “Michael” know what causes the debt to increase: it is because all the money is created as a debt at interest. Banks create the principal they lend, but they do not create the interest they demand. For example, for every person in the U.S.A., there is $20,000 of money in existence... but there is $64,000 of debt!

The only thing that can prevent the debt from growing is to strip private banks of their power to create money as a debt at interest, and to have the U.S. Treasury create all the money for America, debt-and-interest-free.

Balancing the budget or cutting expenses will not solve the problem, since it does not deal with the problem of the creation of money as a debt. In fact, cutting expenses amounts to having less money in circulation, which makes it harder for every American.

The recent welfare reform, passed by the Congress and approved by President Clinton, is a fine example of such misguided cutback policies: because the U.S. Government does not have enough money, the American people will now be able to get welfare for only a maximum of five years, and they cannot receive it for more than two years in a row — they must then find a job. (Whether there are enough jobs available or not is not the concern of the Government. The trend of progress is to make new machines that produce more with less employees, not with more employees.) With other changes (like cutting benefits to resident aliens), this reform means that 40% of those who received welfare benefits until now, will no longer get any with the new plan.

Welfare recipients are an easy target for cutbacks, because their benefits are paid for by the taxes of those who work. Many wage-earners, especially among the middle class, show discontent, not without reason, for it turns out that some people on welfare are better off than those who have to work “by the sweat of their brow.”

The Social Credit dividend (a basic income given every month to every citizen) would be infinitely better than the present welfare system and the reform approved by President Clinton. Contrary to welfare, it would not be financed by the taxpayers' money, but by new money created interest free by the U.S. Treasury. This dividend would be given to every citizen, whether he is employed or not. Those who are employed would therefore not be penalized, since they would receive the dividend plus their wages.

It is obvious that Social Credit is the solution for the United States, as well as to every country in the world. So, how can Social Credit be implemented in the U.S.A.? If the Republicans or the Democrats do not want to include it in their platform, do the Americans have to vote for a new party?

No, there is no need for new parties; only the education of the people is necessary. Once the pressure from the public is strong enough, all the parties will agree with it. A fine example of this can be found in the Goldsborough bill of 1932, which was described by an author as a “Social Credit bill” and “the closest near-miss monetary reform for the establishment of a real sound money system in the United States”:

“An overwhelming majority of the U.S. Congress (289 to 60) favored it as early as 1932, and in one form or another it has persisted since. Only the futile hope that a confident new President (Roosevelt) could restore prosperity without abandoning the credit-money system America had inherited kept Social Credit from becoming the law of the land. By 1936, when the New Deal (Roosevelt's solution) had proved incapable of dealing effectively with the Depression, the proponents of Social Credit were back again in strength. The last significant effort to gain its adoption came in 1938.” (W.E. Turner, Stable Money, p. 167.)

Even the dividend and the compensated discount, two essential parts of Social Credit, were mentioned in this bill, which was the “Goldsborough bill”, after the Democratic Representative of Maryland, T. Allan Goldsborough, who presented it in the House for the first time on May 2, 1932.

Two persons who supported the bill especially hold our attention: Robert L. Owen, Senator of Oklahoma from 1907 to 1925 (a national bank director for 46 years), and Charles G. Binderup, Representative of Nebraska. Owen published an article, in March of 1936, in J. J. Harpell's publication, “The Instructor”, of which Louis Even was the assistant editor. As for Binderup, he gave several speeches on radio in the U.S.A. during the Depression, explaining the damaging effects of the control of credit by private interests. The “Michael” Journal published in the past one of his speeches on Benjamin Franklin's “Colonial Scripts.” (See our September-October, 1993 issue.)

Robert Owen testified in the House, April 28, 1936:

“...the bill which he (Goldsborough) then presented, with the approval of the Committee on Banking and Currency of the House — and I believe it was practically a unanimous report. It was debated for two days in the House, a very simple bill, declaring it to be the policy of the United States to restore and maintain the value of money, and directing the Secretary of the Treasury, the officers of the Federal Reserve Board, and the Reserve banks to make effective that policy. That was all, but enough, and it passed, not by a partisan vote. There were 117 Republicans who voted for that bill (which was presented by a Democrat) and it passed by 289 to 60, and of the 60 who voted against it, only 12, by the will of the people, remain in the Congress.

“It was defeated by the Senate, because it was not really understood. There had not been sufficient discussion of it in public. There was not an organized public opinion in support of it.”

That is the main issue. There are two things that we must remember: Republicans and Democrats alike supported it, so there was no need for a third party or any sort of “Social Credit” party. Moreover, Owen admitted that the only thing that was lacking was the education of the population, a force among the people. That confirms the method used by the “Michael” Journal, advocated by Clifford Hugh Douglas and Louis Even.

The Goldsborough bill was titled: “A bill to restore to Congress its Constitutional power to issue money and regulate the value thereof, to provide monetary income to the people of the United States at a fixed and equitable purchasing power of the dollar, ample at all times to enable the people to buy wanted goods and services at full capacity of the industries and commercial facilities of the United States... The present system of issuing money through private initiative for profit, resulting in recurrent disastrous inflations and deflations, shall cease.”

The bill also made provision for a discount on prices to be compensated to the retailer, and for a national dividend to be issued, beginning at $5 a month (in 1932) to every citizen of the nation. Several groups testified in support of the bill,, stressing the bill provided the means of controlling inflation.

The most ardent opponent in the Senate was Carter Glass, a fierce partisan of the Federal Reserve (private control of money) and a former Secretary of the Treasury. Besides, Henry Morgenthau, then Roosevelt's Secretary of Treasury, who was strongly opposed to any monetary reform, said that Roosevelt's New Deal should be given a trial first.

What mostly helped the opponents to the bill was the near downright ignorance of the money question among the population... and even in the Senate.

Some Senators, knowing nothing about the creation of money (credit) by banks, exclaimed: “The Government cannot create money like that! That will cause runaway inflation!” And others, while admitting the necessity for debt-free money, questioned the necessity for a dividend, or the compensated discount. But all these objections actually disappear after a serious study of Social Credit.

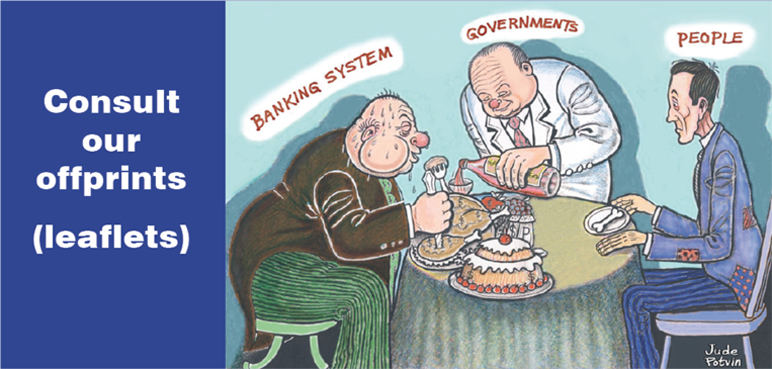

Social Credit would establish a financial system that would serve the human person. It would not only finance the production of goods satisfying human needs, but it would also finance the distribution of these goods to make sure that they reach those who need them. If goods do not reach the consumers, we are producing for nothing. The purpose of production is consumption. This is what Owen had understood:

“In 1932, the Reserve Board vigorously fought the Goldsborough bill, which expressed the overwhelming will of the House of Representatives... There is a great deal of merit, in my opinion, in the principle of distributing our new created money as far as being practicable at the bottom (to the consumers) as was contemplated by Mr. Goldsborough's bill and by Mr. Binderup's bill, because in that way the purchasing power would be produced at the bottom, and without purchasing power at the bottom you cannot have maximum production, because it is vain to produce if you cannot sell.”

This dividend would be based on the two biggest factors to modern production: the inheritance of natural resources and the inventions of past generations, which are both free gifts from God, therefore belonging to all. Far from being an incitement to idleness, the dividend would allow people to allocate themselves to those jobs to which they are best suited. (Moreover, jobs would be more secure, once consumers are guaranteed enough purchasing power.)

There is also a technical argument in favor of the dividend: the gap between purchasing power and prices, which was explained by Scottish engineer Clifford Hugh Douglas (the inventor of Social Credit) as the “A + B theorem”: .

Economists maintain that production automatically finances consumption, that is to say, that the wages distributed to the consumers are sufficient to buy all of the available goods and services. They are wrong, since facts prove just the opposite: Wages are only one part of the price of a finished good. The total cost price of any given finished good is made up of several other factors: payments for materials, taxes, banking charges, charges for depreciation, etc.

Douglas calls “A” the payments made to individuals (wages), and “B” the payments made to other organizations (for raw material, etc.). So “A” is the sum of the salaries, and “B” the sum of other costs. It is obvious that the retail price of any product must include all of the costs (A + B), and that A cannot buy A + B, that wages cannot buy all of the production. For any period of time, the rate of flow of prices created is always greater than the rate of flow of purchasing power distributed.

So a direct financing of consumers is needed, by some other channel than wages. (Since wages are included in prices, wage increases will settle nothing, bringing automatically a rise in prices.) An additional income — at least equivalent to “B”, is therefore necessary. The Social Crediters call this income a dividend.

Since the dividend has not yet been implemented in the present system, there should be, theoretically, a growing mountain of unsold goods. If the system keeps going, and if goods are sold just the same, it is because one has, instead, a growing mountain of debt!

There are two ways to make the total of the prices and the total of the purchasing power in the hands of the consumers to correspond: either lower the prices, or increase the purchasing power. Social Credit would do both, without harming anyone.

In the present system, it is impossible to lower the prices without harming the producers, and it is impossible to increase the purchasing power of the consumers without raising the prices. The additional money must therefore not come from the wages, but from a different source: it is the Social Credit dividend. And the mechanism to lower the prices is called the “compensated discount” — a discount on the prices of every retail goods, which would be compensated to the retailer by the U.S. Treasury. This discount is meant to prevent any possibility of inflation.

Inflation also means too much money in relation to products. In a Social Credit system, there would be no danger of inflation, since there would be a constant balance between money and goods: money would be issued as goods are made, and be withdrawn from circulation as goods are consumed.

All this is explained very briefly, but our purpose is to show that Social Credit is not an utopia, but a scientific system based on facts that can be applied immediately in any country. Social Credit only wants to “make financially possible what is physically possible.” We encourage our readers to start studying Social Credit, and above all, to make it known to others, by diffusing and soliciting subscriptions to the “Michael” Journal. (Details on the technical aspects of Social Credit are available in Louis Even's book, In This Age of Plenty, and in our two booklets, A Sound And Effective Financial System and What Do We Mean By Real Social Credit?.)

Let us bring an end to this article with the quotations of two great American citizens.

Thomas Edison: “Throughout our history some of America's greatest men have sought to break the Hamiltonian imprint (Alexander Hamilton's debt-money policy) on our monetary policy in order to substitute a stable money supply measured to the nation's physical requirements. Lack of public and official understanding, combined with the power of banking interests who have imagined a vested interest in the present chaotic system, have so far thwarted every effort.

“Don't allow them to confuse you with the cry of `paper money.' The danger of paper money is precisely the danger of gold — if you get too much it is no good. There is just one rule for money and that is to have enough to carry on all the legitimate trade that is waiting to move. Too little and too much are both bad. But enough to move trade, enough to prevent stagnation, on the one hand, not enough to permit speculation, on the other hand, is the proper ratio...

“If the United States will adopt this policy of increasing its national wealth without contributing to the interest collector — for the whole national debt is made up of interest charges — then you will see an era of progress and prosperity in this country such as could never have come otherwise.”

And a call from Henry Ford: “The youth who can resolve the money question will do more for the world than all the professional soldiers of history.”

Young people, have you understood? Join the ranks of the apostles of the “Michael” Journal, for the sake of your country and fellow citizens. The Pilgrims of Saint Michael need you; they are waiting for you!

| Previous chapter - The History of Banking Control | Next chapter - The Aim of the Financiers |

Alain Pilote has been the editor of the English edition of MICHAEL for several years. Twice a year we organize a week of study of the social doctrine of the Church and its application and Mr. Pilote is the instructor during these sessions.

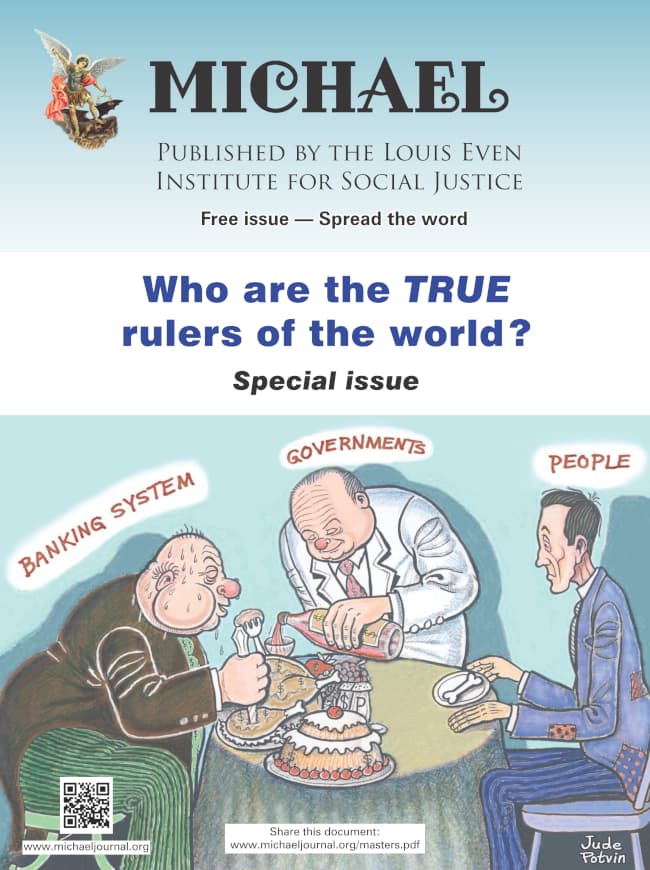

In this special issue of the journal, MICHAEL, the reader will discover who are the true rulers of the world. We discuss that the current monetary system is a mechanism to control populations. The reader will come to understand that "crises" are created and that when governments attempt to get out of the grip of financial tyranny wars are waged.

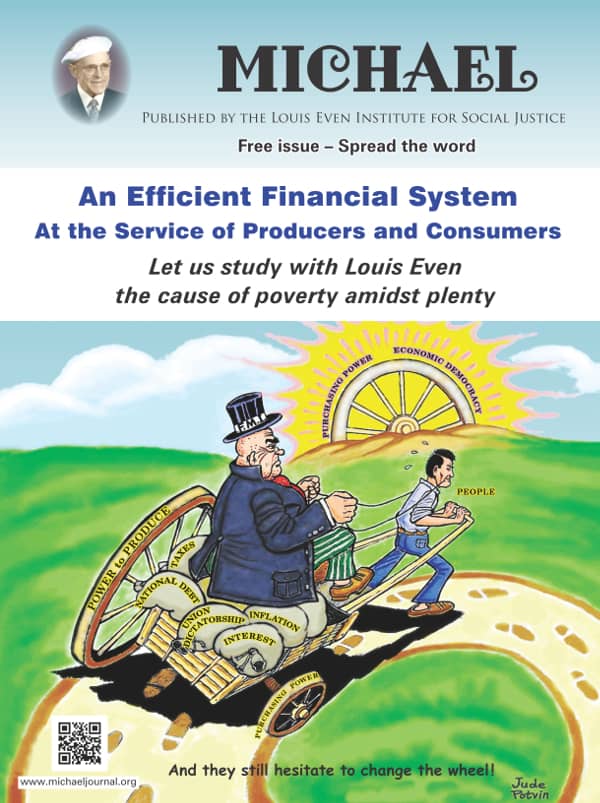

In this special issue of the journal, MICHAEL, the reader will discover who are the true rulers of the world. We discuss that the current monetary system is a mechanism to control populations. The reader will come to understand that "crises" are created and that when governments attempt to get out of the grip of financial tyranny wars are waged. An Efficient Financial System, written by Louis Even, is for the reader who has some understanding of the Douglas Social Credit monetary reform principles. Technical aspects and applications are discussed in short chapters dedicated to the three propositions, how equilibrium between prices and purchasing power can be achieved, the financing of private and public production, how a Social Dividend would be financed, and, finally, what would become of taxes under a Douglas Social Credit economy. Study this publication to better grasp the practical application of Douglas' work.

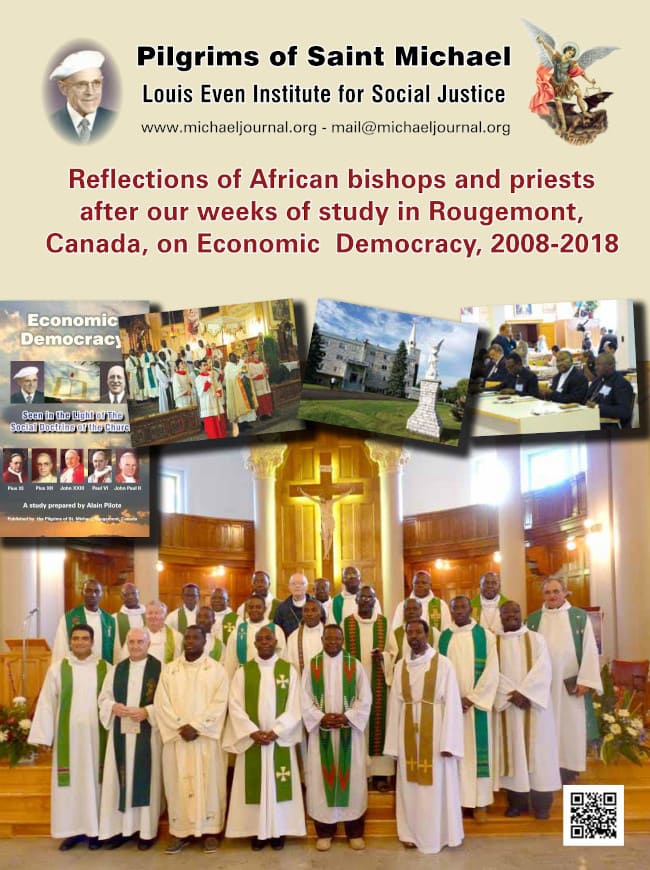

An Efficient Financial System, written by Louis Even, is for the reader who has some understanding of the Douglas Social Credit monetary reform principles. Technical aspects and applications are discussed in short chapters dedicated to the three propositions, how equilibrium between prices and purchasing power can be achieved, the financing of private and public production, how a Social Dividend would be financed, and, finally, what would become of taxes under a Douglas Social Credit economy. Study this publication to better grasp the practical application of Douglas' work.  Reflections of African bishops and priests after our weeks of study in Rougemont, Canada, on Economic Democracy, 2008-2018

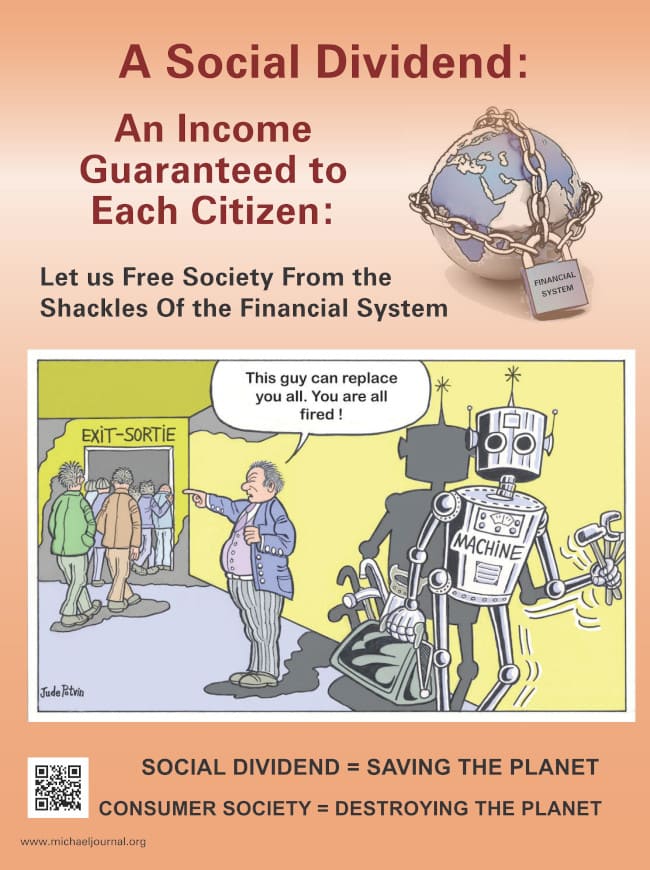

Reflections of African bishops and priests after our weeks of study in Rougemont, Canada, on Economic Democracy, 2008-2018 The Social Dividend is one of three principles that comprise the Social Credit monetary reform which is the topic of this booklet. The Social Dividend is an income granted to each citizen from cradle to grave, with- out condition, regardless of employment status.

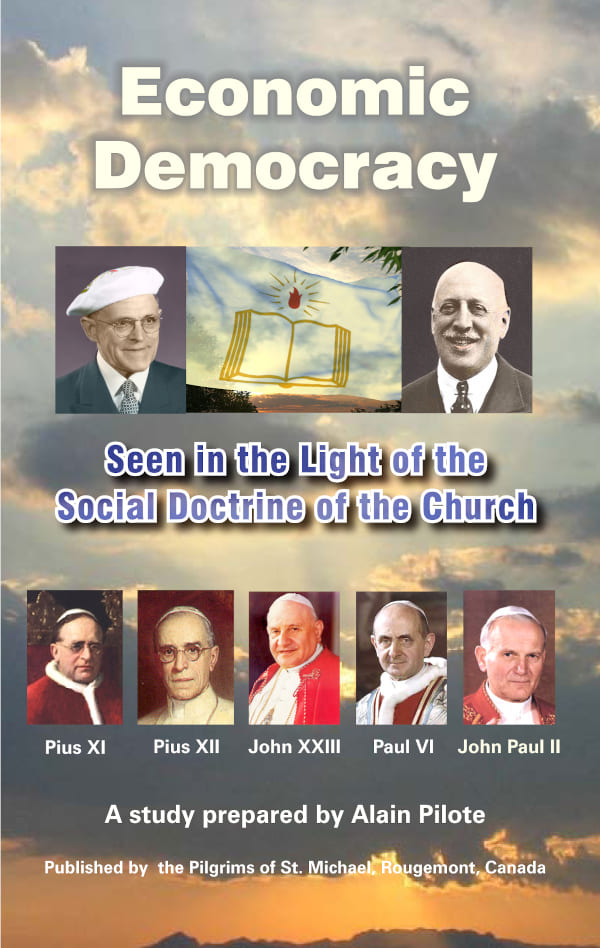

The Social Dividend is one of three principles that comprise the Social Credit monetary reform which is the topic of this booklet. The Social Dividend is an income granted to each citizen from cradle to grave, with- out condition, regardless of employment status. Economic Democracy is a book to explain Social Credit in lessons presented in logical order so it may be easier to the reader to grab the main principles of Social Credit rapidly and somehow easily.

Economic Democracy is a book to explain Social Credit in lessons presented in logical order so it may be easier to the reader to grab the main principles of Social Credit rapidly and somehow easily. In This Age of Plenty deals with Social Credit, but it does not exhaust the topic. Social Credit principles address social and political matters, as well as, or even more so, than economics and will put civilization on a new course.

In This Age of Plenty deals with Social Credit, but it does not exhaust the topic. Social Credit principles address social and political matters, as well as, or even more so, than economics and will put civilization on a new course. From Debt to Prosperity outlines briefly the economic analysis and constructive proposals known as Social Credit.

From Debt to Prosperity outlines briefly the economic analysis and constructive proposals known as Social Credit.

Rougemont Quebec Monthly Meetings

Every 4th Sunday of every month, a monthly meeting is held in Rougemont.

Subscribe

Subscribe