The legislative power resides in parliaments, since this is where laws are discussed and voted upon.

The legislative power resides in parliaments, since this is where laws are discussed and voted upon.

The executive power resides in the offices of ministers, since it is they — the Prime Minister and his Cabinet — who make the decisions that are carried out by the civil servants.

The judiciary power resides in the courts, since that is where the judges exercise their function.

And where does the superpower, the monetary power, reside?

The monetary power resides in the banks. It is in the banks that financial credit is in fact created and where it dies.

When a bank grants a loan, either to a contractor, a retailer, or to a government, new financial credit is created. The banker credits the borrower's account with the loan granted, just as if the borrower had deposited that amount. But the borrower did not bring nor did he deposit any money, since he came to the bank to get money he did not have.

The borrower will now be able to issue cheques on this account that he did not have when he entered the bank, but that he now has upon leaving the bank.

None of the bank's other customers' accounts were decreased. This is therefore a new account, added to the accounts that already existed. The total credits in the total accounts of the bank are therefore increased by the amount of this new account. There is therefore an increase in financial credit, new money that goes into circulation via the cheques the borrower writes based on this new credit.

In contrast, when a borrower comes to the bank to repay his loan, that is, the credit he had borrowed previously, the quantity of credit in circulation will be decreased accordingly: An amount of blood is being removed from the economic body.

A simple bookkeeping operation, made with one stroke of the pen, created financial credit. Another simple bookkeeping operation, when the loan is repaid, cancels out and sends this credit to the grave.

It is easy to see that if, during a given period of time, the total of the loans exceeds the total of repayments, then there are more credits put into circulation than there are credits cancelled. Inversely, if the total of the repayments exceeds the total of the loans, it causes a period of reduction in the credit being circulated.

If the reduction period persists, the whole economic body is affected by it: it is called a crisis — a crisis caused by a restriction of credit.

Thus these periods of increase and of decrease are not due to hazard but to the actions of the banks.

Since the borrower must pay back more than the amount that was lent to him, because of the interest charged, he must withdraw from circulation more money than he has put into it. For this reason, he must withdraw from circulation money in excess, money that was put into circulation by other borrowers. Since all new credit is issued by the banks, under the condition of paying back more money than the amounts that were granted, new borrowers will have to be found. The latter will face a double difficulty in repaying their loans, since they too must find excess money to cover their own interests, within a circulation of money that has already been depleted by the first borrowers.

And the same applies to future borrowers. Repayments become practically impossible. Banks then turn down new loans, thus slowing down the whole economic life. They see to it that the blame for this be placed upon the population which suffers from this state of affairs.

In order for the flow of credit required for economic life to start again, a string of loans will have to be set in motion again, giving rise to an ever increasing string of debts.

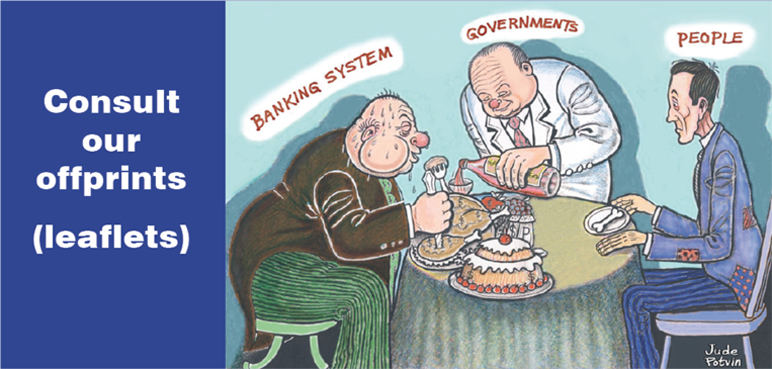

The present banking system is the instrument used by the monetary superpower to maintain its supremacy over nations and their governments, aided in the process by the ridiculous politico-financial rule that binds the distribution of purchasing power to employment, in a production system that requires fewer and fewer hands to supply the basic needs.

You must not conclude from this that your local banker is part of this dictatorship. He is only a subordinate who is most likely unaware that when he enters loans in the ledgers of his bank, he creates credit, and that the repayments entered in his bank's ledger destroy this credit.

Nor does he decree the restrictions of credit that deprive the economy of its life-blood. He only follows the orders he receives without measuring the consequences.

You may still hear attarded scholars deny that the volume of credit in circulation depends upon the action of the banks. These backward scholars, who resist the obvious, are an invaluable support to the superpower, through their ignorance — if it is really ignorance on their part, or through vested interests that bind them, or through their collusion with a power which can bring them easy promotions.

High ranking bankers, on the other hand, know very well that financial credit, which makes up the bulk of modern money, is created and cancelled in bank ledgers.

A distinguished British banker, the Right Honourable Reginald McKenna, one-time British Chancellor of the Exchequer, and Chairman of the Midland Bank, one of the Big Five (five largest banks of England), addressed an annual general meeting of the shareholders of the bank, on January 25, 1924, and said (as recorded in his book, Post-War Banking):

“I am afraid the ordinary citizen will not like to be told that the banks can, and do, create and destroy money. The amount of finance in existence varies only with the action of the banks in increasing or decreasing deposits and bank purchases. We know how this is effected. Every loan, overdraft, or bank purchase creates a deposit, and every repayment of a loan, overdraft, or bank sale destroys a deposit.”

Having been Minister of Finance, McKenna knew full well where the bigger of the two powers resided — the power of the banks and that of the sovereign government of the country. And he stated frankly, a virtue seldom shown by bankers at his level:

“They (the banks) control the credit of the nation, direct the policies of governments, and keep in the palm of their hands the destinies of the peoples.”

This statement is in complete agreement with what Pope Pius XI wrote in his Encyclical Letter Quadragesimo Anno, in 1931, about “those who, because they hold and control money, are able also to govern credit and determine its allotment, for that reason supplying, so to speak, the lifeblood to the entire economic body, and grasping, as it were, in their hands the very soul of production, so that no one dare breathe against their will"

| Previous chapter - A superpower Dominates Governments | Next chapter - Liberal Leader Mackenzie King Said in 1935 |

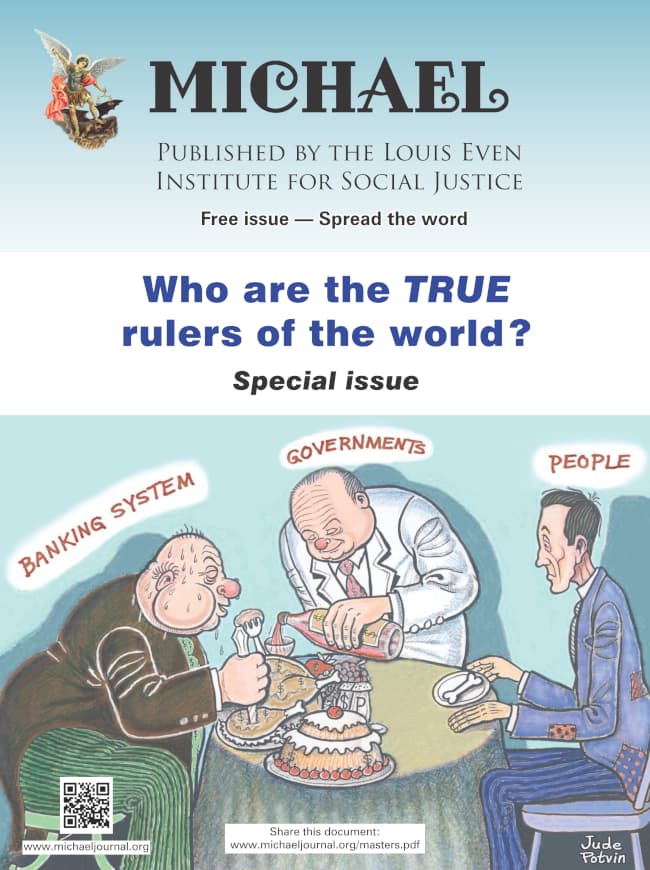

In this special issue of the journal, MICHAEL, the reader will discover who are the true rulers of the world. We discuss that the current monetary system is a mechanism to control populations. The reader will come to understand that "crises" are created and that when governments attempt to get out of the grip of financial tyranny wars are waged.

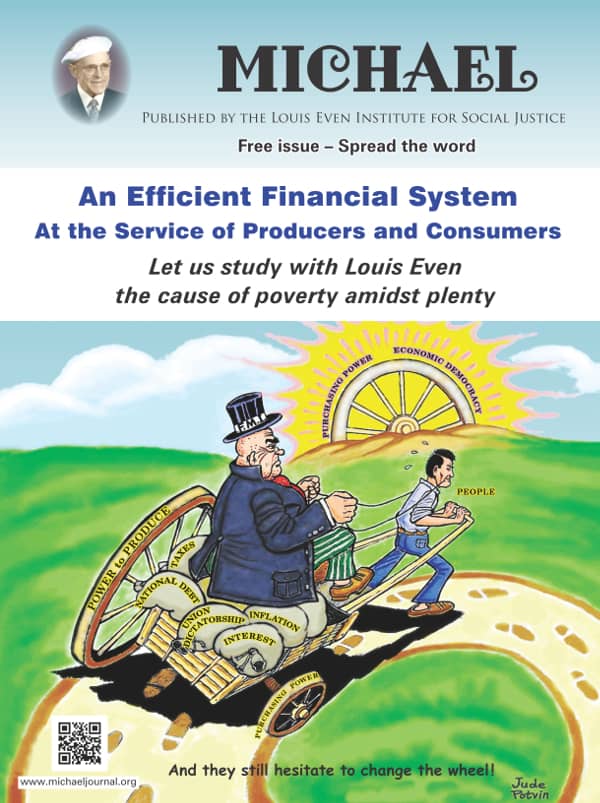

In this special issue of the journal, MICHAEL, the reader will discover who are the true rulers of the world. We discuss that the current monetary system is a mechanism to control populations. The reader will come to understand that "crises" are created and that when governments attempt to get out of the grip of financial tyranny wars are waged. An Efficient Financial System, written by Louis Even, is for the reader who has some understanding of the Douglas Social Credit monetary reform principles. Technical aspects and applications are discussed in short chapters dedicated to the three propositions, how equilibrium between prices and purchasing power can be achieved, the financing of private and public production, how a Social Dividend would be financed, and, finally, what would become of taxes under a Douglas Social Credit economy. Study this publication to better grasp the practical application of Douglas' work.

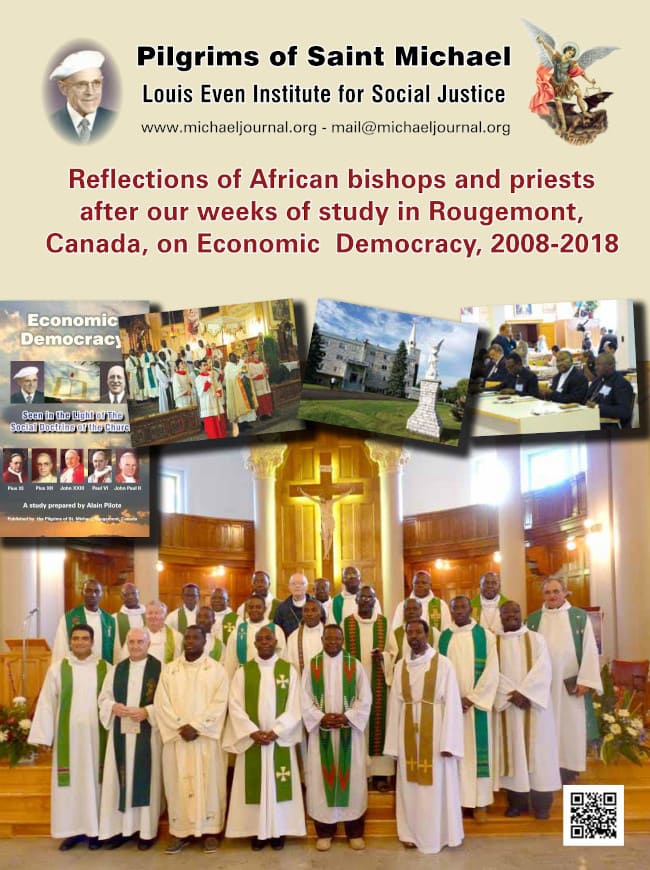

An Efficient Financial System, written by Louis Even, is for the reader who has some understanding of the Douglas Social Credit monetary reform principles. Technical aspects and applications are discussed in short chapters dedicated to the three propositions, how equilibrium between prices and purchasing power can be achieved, the financing of private and public production, how a Social Dividend would be financed, and, finally, what would become of taxes under a Douglas Social Credit economy. Study this publication to better grasp the practical application of Douglas' work.  Reflections of African bishops and priests after our weeks of study in Rougemont, Canada, on Economic Democracy, 2008-2018

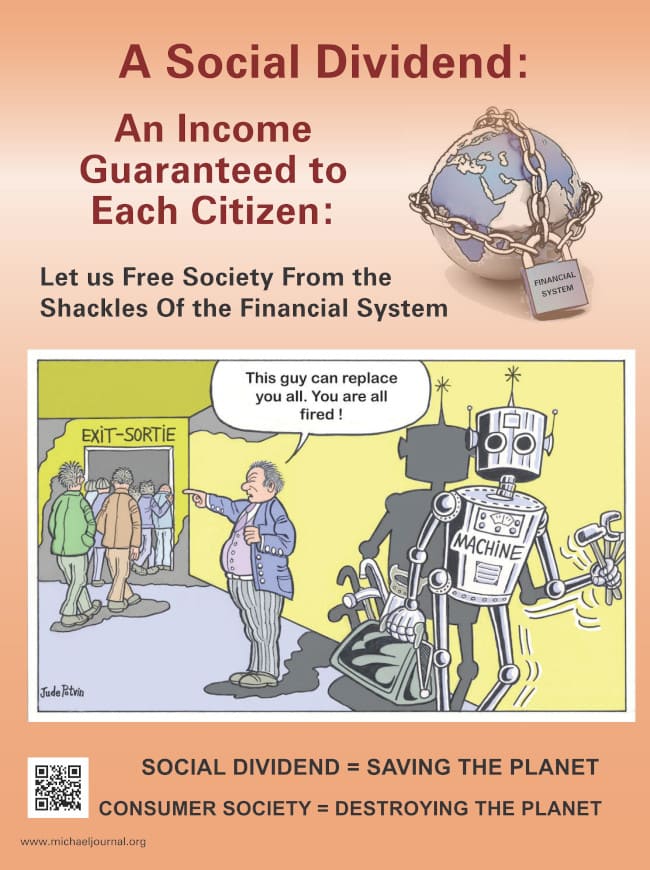

Reflections of African bishops and priests after our weeks of study in Rougemont, Canada, on Economic Democracy, 2008-2018 The Social Dividend is one of three principles that comprise the Social Credit monetary reform which is the topic of this booklet. The Social Dividend is an income granted to each citizen from cradle to grave, with- out condition, regardless of employment status.

The Social Dividend is one of three principles that comprise the Social Credit monetary reform which is the topic of this booklet. The Social Dividend is an income granted to each citizen from cradle to grave, with- out condition, regardless of employment status. Economic Democracy is a book to explain Social Credit in lessons presented in logical order so it may be easier to the reader to grab the main principles of Social Credit rapidly and somehow easily.

Economic Democracy is a book to explain Social Credit in lessons presented in logical order so it may be easier to the reader to grab the main principles of Social Credit rapidly and somehow easily. In This Age of Plenty deals with Social Credit, but it does not exhaust the topic. Social Credit principles address social and political matters, as well as, or even more so, than economics and will put civilization on a new course.

In This Age of Plenty deals with Social Credit, but it does not exhaust the topic. Social Credit principles address social and political matters, as well as, or even more so, than economics and will put civilization on a new course. From Debt to Prosperity outlines briefly the economic analysis and constructive proposals known as Social Credit.

From Debt to Prosperity outlines briefly the economic analysis and constructive proposals known as Social Credit.

Rougemont Quebec Monthly Meetings

Every 4th Sunday of every month, a monthly meeting is held in Rougemont.

Subscribe

Subscribe