We have already touched on the old idea that gold is the basis of money. It is true that gold, itself only one commodity among many, was used as money for centuries before the present Age of Power was ever dreamed of. But it is indeed strange to find financiers today still believing that this one commodity is the only basis of money in our complex twentieth century world of business. «Money is gold, and nothing else,» said J. P. Morgan.1

Despite the absurdity of this statement many people have accepted it, and its acceptance has serious consequences.

Gold is a commodity whose supply is strictly limited; indeed, it is distinguished chiefly by its scarcity. Compared with the needs of industry and business gold is too scarce to be practical as money. In fact in this country it is legally a criminal offense for individuals to own coined gold. But if the value of money is based on gold alone, it is an easy step from thinking of the commodity, gold, to thinking of money itself as a commodity. And the real scarcity of gold can easily persuade many of us to accept quite naturally a corresponding scarcity of money.

If all the world’s gold were sunk tomorrow in the middle of the Atlantic we could still write cheques. How long will people tolerate this illusion of gold and money? “Do you think that civilized countries have from experience and knowledge of economics reached a stage where they could drop the fiction, unreality, and chaotic state of a currency based on gold, and adopt a money back of which is real useful wealth...? This gold money ... is a fiction.”2

How is this fiction transformed into a fact of painful reality? We must remember that financiers today deal in money just as most of us deal in goods, except that they need very little raw material to manufacture it. We regard the flour or coal we deal in as a commodity, and when it is scarce we know that its value will rise. Just so financiers have come to regard money, and today that means credit, as their commodity, and quite logically they wish to keep it relatively scarce. For only so will it command great power over goods.

Since the value of money as a commodity is thus raised by limiting its supply, financiers naturally frown on any suggestion that it could be more plentiful. The supply of money is limited by the self-made rules of our existing financial system, but this is concealed from the public. On the contrary, the financial fraternity has woven in the public mind a deceptive illusion about the scarcity of Money.

We are beginning to realize something of what has happened. “...Arising out of this it would seem that financial credit is restricted because, at the present time, money is dealt in as a commodity, and by keeping money in short supply its value as a commodity is enhanced. For this reason it seems undesirable that financial policy should be in the control of a private monopoly whose interests are not identical with the interests of the community as a whole.”3

The fact that this scarcity is a pure illusion has been repeatedly proven. We know by the testimony of bankers that banks create and destroy 90% of our money by a method that in essence amounts to nothing but bookkeeping. They are dominated in this process by private gain. But because money is issued as debt and kept in artificial scarcity by this singular illusion, it is not available in sufficient quantity to express the demand for goods which, as we have seen, is its prime purpose. The illusion of scarcity thus frustrates the fulfillment of the purpose of money. A constant shortage of purchasing power inevitably follows and the needs and desires of all of us as consumers must to this extent go unsatisfied. So long as the subtle illusion of scarcity is sustained by financial power this scarcity will continue.

A very interesting sidelight on this situation is given by the confidential circulars issued in 1877 by leading New York bankers to all national banks. “To repeal the law enacting national bank notes or to restore to circulation the government issue of money,” the banks were told, “will be to provide the people with money and therefore seriously affect your individual profits as bankers and lenders.” And again: “You will at once retire one-third of your circulation and call in one- half of your loans. Be careful to make a money stringency felt among your patrons, especially among influential business men.”4

Well, the stringency has many times been felt. We know its painful power. But it has been a boomerang hastening the downfall of finance itself, to say nothing of its devastating effect upon the personal pocketbooks of the nation’s shoppers.5

1) Testimony before the Pujo Committee, 1912. Cf. Supreme Court decision, Feb. 18, 1935.

2) Thomas A. Edison, quoted in TODAY, Jan. 13, 1934.

3) Report of the Economic Crisis Committee, Southampton Chambre of Commerce, England, 1933.

4) Arthur Kitson, Industrial Depression

Issuing it as a debt, the banking system can recall and destroy credit-money at will. Exercise of this power produced the panic of 1929. Deposits produced by bank creations of private money, lent as created, were contracted by wholesale. This started a shrinkage in demand back loans and deposits of 20 billions of dollars. It has resulted in a reduction of the volume of check-money turnover from 1200 billions in 1929 to less than 400 billions in 1933. This amounts to an annihilation of two-thirds of the money for the transaction of business.

Such deliberate shrinkage of private money by the contraction of credit and bank loans and bank deposits, produced the depression of 1907. Again in May, 1920, a meeting was held in secret by members of the Federal Reserve board, the Federal Reserve Advisory Council, and 36 Class A directors of the Federal Reserve banks which are owned by the private member banks; in this meeting, after an all-day discussion, it was determined to contract the nation’s credit and currency.

As a consequence, beginning in July, 1920, the commodity price level declined from 166 to 93, as compared with the price level of 1913. Agricultural products fell by more than one-half while the value of farms declined from a gross of 79 billion to 58½ billions.

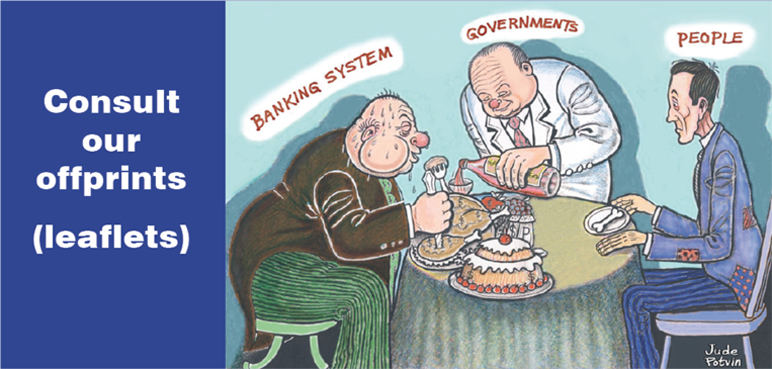

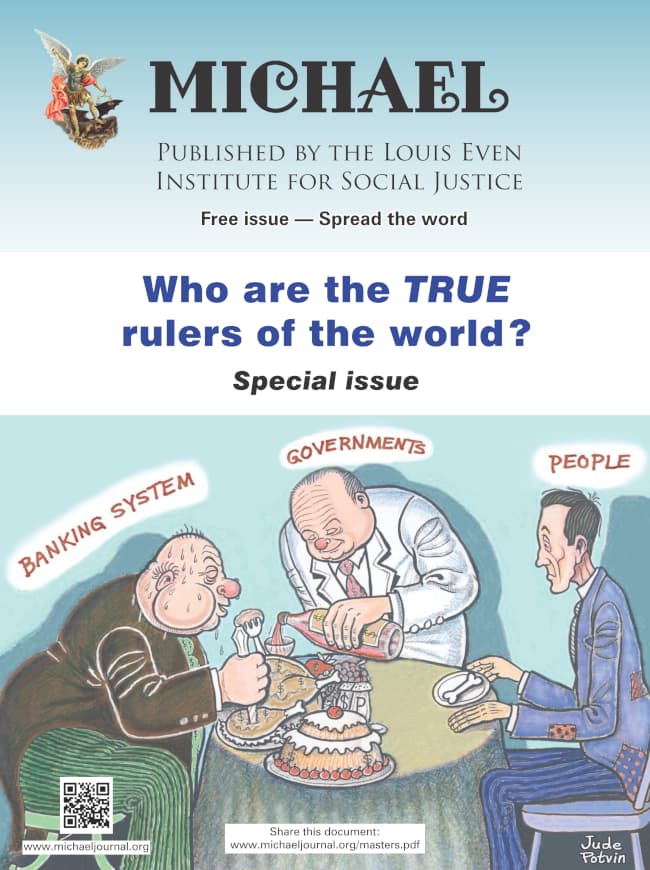

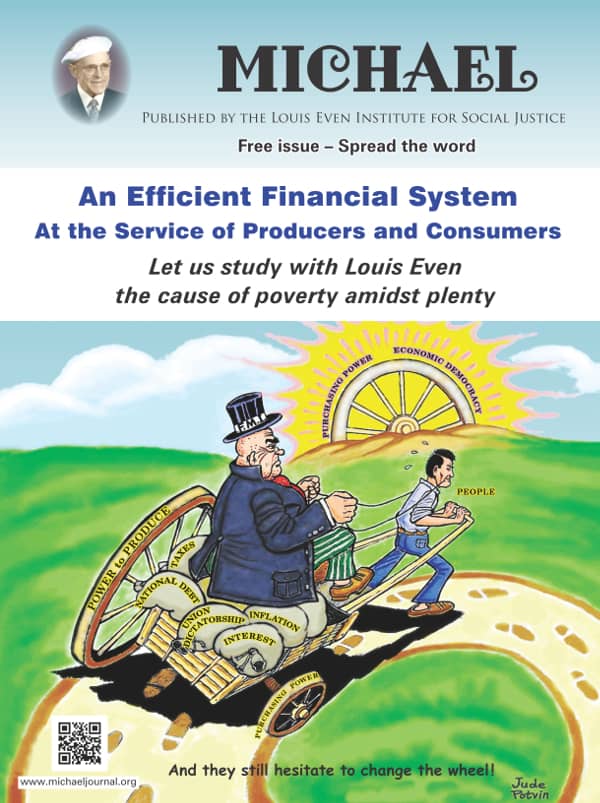

In this special issue of the journal, MICHAEL, the reader will discover who are the true rulers of the world. We discuss that the current monetary system is a mechanism to control populations. The reader will come to understand that "crises" are created and that when governments attempt to get out of the grip of financial tyranny wars are waged.

In this special issue of the journal, MICHAEL, the reader will discover who are the true rulers of the world. We discuss that the current monetary system is a mechanism to control populations. The reader will come to understand that "crises" are created and that when governments attempt to get out of the grip of financial tyranny wars are waged. An Efficient Financial System, written by Louis Even, is for the reader who has some understanding of the Douglas Social Credit monetary reform principles. Technical aspects and applications are discussed in short chapters dedicated to the three propositions, how equilibrium between prices and purchasing power can be achieved, the financing of private and public production, how a Social Dividend would be financed, and, finally, what would become of taxes under a Douglas Social Credit economy. Study this publication to better grasp the practical application of Douglas' work.

An Efficient Financial System, written by Louis Even, is for the reader who has some understanding of the Douglas Social Credit monetary reform principles. Technical aspects and applications are discussed in short chapters dedicated to the three propositions, how equilibrium between prices and purchasing power can be achieved, the financing of private and public production, how a Social Dividend would be financed, and, finally, what would become of taxes under a Douglas Social Credit economy. Study this publication to better grasp the practical application of Douglas' work.  Reflections of African bishops and priests after our weeks of study in Rougemont, Canada, on Economic Democracy, 2008-2018

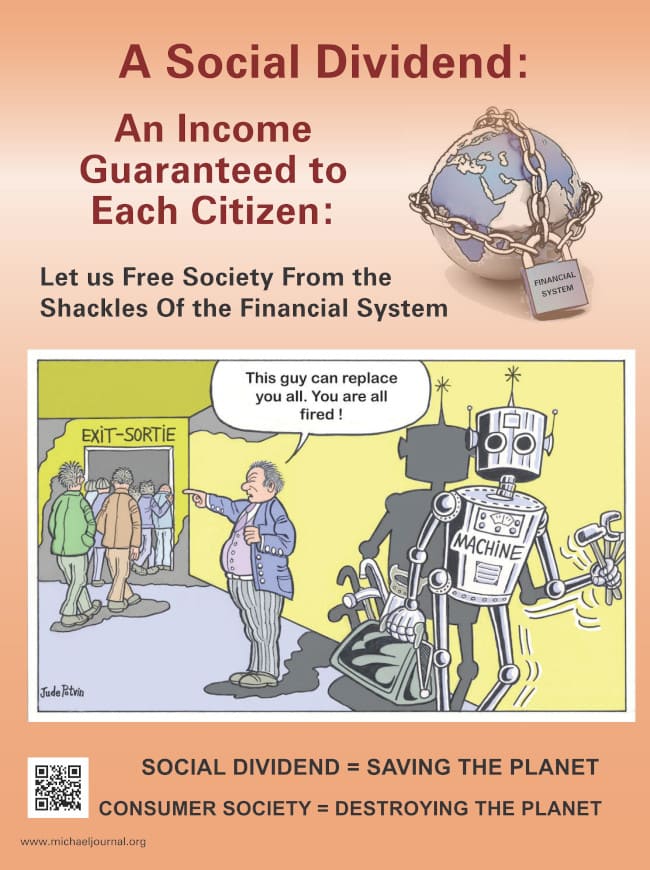

Reflections of African bishops and priests after our weeks of study in Rougemont, Canada, on Economic Democracy, 2008-2018 The Social Dividend is one of three principles that comprise the Social Credit monetary reform which is the topic of this booklet. The Social Dividend is an income granted to each citizen from cradle to grave, with- out condition, regardless of employment status.

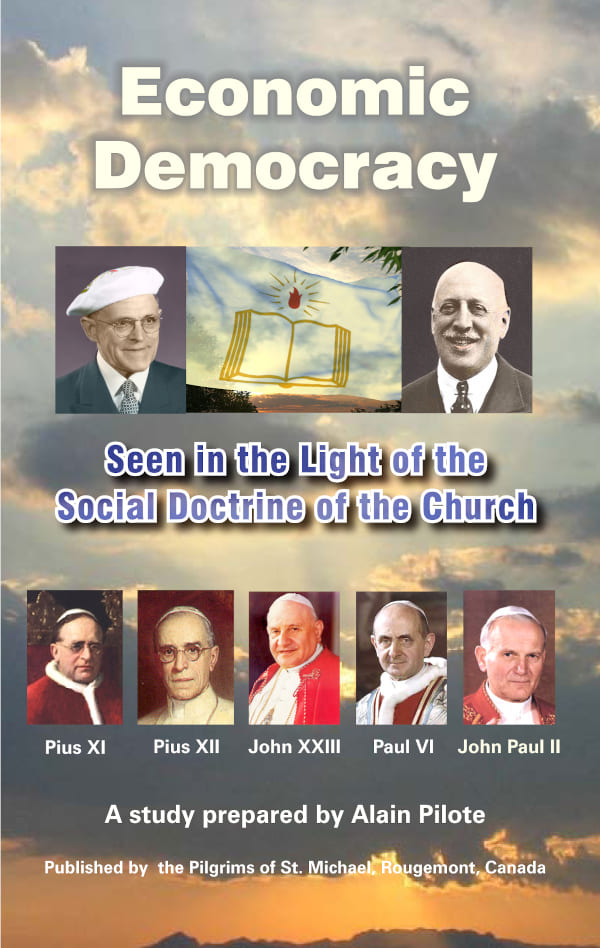

The Social Dividend is one of three principles that comprise the Social Credit monetary reform which is the topic of this booklet. The Social Dividend is an income granted to each citizen from cradle to grave, with- out condition, regardless of employment status. Economic Democracy is a book to explain Social Credit in lessons presented in logical order so it may be easier to the reader to grab the main principles of Social Credit rapidly and somehow easily.

Economic Democracy is a book to explain Social Credit in lessons presented in logical order so it may be easier to the reader to grab the main principles of Social Credit rapidly and somehow easily. In This Age of Plenty deals with Social Credit, but it does not exhaust the topic. Social Credit principles address social and political matters, as well as, or even more so, than economics and will put civilization on a new course.

In This Age of Plenty deals with Social Credit, but it does not exhaust the topic. Social Credit principles address social and political matters, as well as, or even more so, than economics and will put civilization on a new course. From Debt to Prosperity outlines briefly the economic analysis and constructive proposals known as Social Credit.

From Debt to Prosperity outlines briefly the economic analysis and constructive proposals known as Social Credit.

Rougemont Quebec Monthly Meetings

Every 4th Sunday of every month, a monthly meeting is held in Rougemont.

Subscribe

Subscribe